Your Phone Generates $390 Billion for Big Tech Every Year. You Earn $0. And Inflation at 3.8% Is Quietly Eroding Every RMD You Take in Cash.

URGENT: Is this the “Starlink of Smartphones”?

SpaceX changed how we reach the stars. Starlink changed how the world connects to the internet. But there is still one massive problem: The devices in our pockets are still “dumb.” Ordinary smartphones cost over $1,000 and pay you exactly $0.00. They are a drain on your wallet in an era where technology should be working for you.

Enter Mode Mobile ($MODE). Just as Starlink brought the internet to the masses, Mode is bringing “EarnOS” to the world’s 7 billion smartphones. It’s the first device designed to put money in your pocket by rewarding you for every song, game, and charge.

With $115M in revenue and $11.8M as EBITDA and a growth rate of 32,481%, Deloitte just named them the #1 fastest-growing software company in North America.

They’ve already reserved their Nasdaq ticker ($MODE). This is your chance to own a piece of the “Triple Threat” of modern tech — at $0.50 per share slams shut. Don’t just watch the revolution on the news.

| Secure your shares at $0.50/share before price changes on 05/29! |

Please read the offering circular and related risks at invest.modemobile.com. This is a paid advertisement for Mode Mobile’s Regulation A+ Offering. Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur. The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period. Pro forma revenue and EBITDA, includes full year numbers of the businesses acquired throughout 2025.

In-app advertising spending will reach $390 billion worldwide in 2026. The mobile app economy is projected at $1.2 trillion. There are 4.69 billion smartphone users globally — an increase of 440 million from 2025 alone. Users spend an average of $285,000 per minute on apps. And 98% of all mobile app revenue comes from free applications, meaning the value is being extracted through your attention, your data, and your engagement — not through a price you choose to pay.

What this means for your retirement accounts: The smartphone you carry generates enormous value for the companies that capture your attention. Google, Meta, Apple, and Amazon collectively earn over $500 billion per year from digital advertising and app-store commissions. The average revenue per user is $4.52 globally. But none of that value flows back to you. Your phone costs you $1,000+ to buy and hundreds per year in service fees, and in return it monetizes your attention for someone else’s profit. The structural question is whether a company that flips this model — turning the phone from a cost center into an earning device — captures the next wave of value creation in the $1.2 trillion app economy.

Why this matters if you hold index funds: The attention economy is not rate-sensitive. People check their phones 96 times per day regardless of what the Fed does. Screen time has never declined year-over-year. The companies positioned to let users earn from their own phone activity are building revenue models that operate outside the interest rate cycle, outside the SpaceX forced rebalancing, and outside the macro pressures that threaten traditional portfolios. Pre-IPO positions in this space are how protection-first investors access the $390 billion advertising market without being subjected to public market mechanics.

The $390 billion flows to Big Tech. Your phone earns $0. The company that changes this equation — and has already reserved its Nasdaq ticker — is where the structural shift begins.

[AD] SpaceX changed how we reach the stars. Starlink changed how the world connects to the internet. But there is still one massive problem: The devices in our pockets are still “dumb.” Ordinary smartphones cost over $1,000 and pay you exactly $0.00. Enter Mode Mobile ($MODE). Just as Starlink brought the internet to the masses, Mode is bringing “EarnOS” to the world’s 7 billion smartphones. With $115M in revenue and $11.8M as EBITDA and a growth rate of 32,481%, Deloitte just named them the #1 fastest-growing software company in North America. They’ve already reserved their Nasdaq ticker ($MODE). Claim your stake in the $MODE era today.

If You’re 73 or Older, Your Required Minimum Distributions Are Being Eroded by 3.8% Inflation Every Time You Take Them in Cash

Why this matters if you’re retired or near retirement: The Motley Fool reported in March 2026 that SECURE 2.0 has made three significant RMD changes: the age increased to 73 (75 in 2033), the penalty dropped to 25%, and Roth 401(k)/403(b) plans are now exempt from RMDs. Charles Schwab noted that the QCD limit increased to $111,000 for 2026, allowing charitable donations from IRAs to satisfy RMD requirements. But none of these changes address the fundamental problem: if you take your RMD in cash and inflation is at 3.8%, every dollar you withdraw has less purchasing power than when you earned it. The protection is not in the timing of the withdrawal. It is in what the withdrawal is denominated in.

IRS Code 408(m) Allows a Different Approach. Most Retirees Have Never Heard of It.

What this means for your retirement accounts: IRS Code 408(m) defines specific types of gold, silver, platinum, and palladium that can be held inside a self-directed IRA. The process uses a direct trustee-to-trustee transfer with no taxable event, no early-withdrawal penalty, and no disruption to the existing account. The gold sits in an IRS-approved depository. The tax advantages remain intact. And the allocation provides genuine non-correlation — an asset whose value derives from scarcity and universal recognition rather than earnings multiples, interest rate policy, or currency stability. Gold has risen 144% since the rate cut cycle began in 2024. At 3.8% CPI, it is doing exactly what it is supposed to do: preserving purchasing power while cash erodes.

Your RMD Strategy May Be Bleeding Money

If you’re near or over 73, this matters. Most retirees take their Required Minimum Distributions (RMDs) the default way. In cash. And that’s where the problem starts.

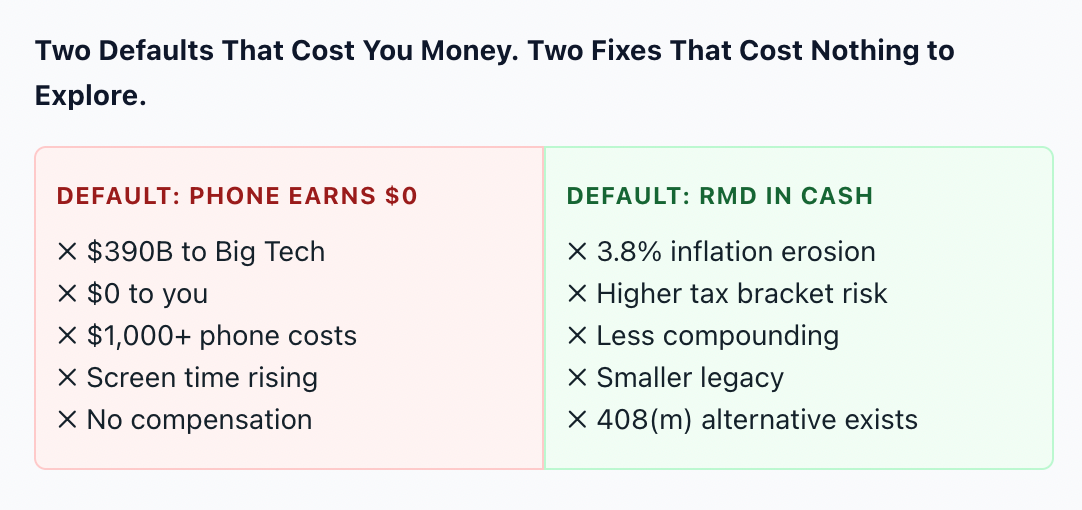

Because taking RMDs the wrong way can mean: More taxes for Washington. Less compounding for you. A smaller legacy for your family.

What most retirees don’t realize is that IRS Code 408(m) allows RMDs to be handled differently — in a way that may help protect more of what you’ve earned. But timing matters. Once the distribution hits your account, options shrink fast.

We created a free guide explaining: The #1 RMD trap. Why inflation quietly erodes cash distributions. How some retirees are repositioning before it’s too late.

| Download your FREE RMD Guide here → |

Your Phone Should Earn. Your RMD Should Protect. Both Fixes Start with Changing the Default.

The Americans who are protecting their wealth in 2026 are the ones who rejected the defaults: the default that your phone earns nothing while Big Tech captures $390 billion from your attention, and the default that your RMD comes out in cash while 3.8% inflation erodes its value every year. Both defaults cost you money. Both have alternatives. And both alternatives start with a free guide that explains what most people never learn.

IRS Rule Most Retirees Ignore

If you’re near or over 73, your RMD strategy may be bleeding money. IRS Code 408(m) allows RMDs to be handled differently. CPI is at 3.8%. Cash distributions erode every year. A free guide explains the #1 RMD trap and how some retirees are repositioning.

Bottom Line

In-app advertising will reach $390 billion globally in 2026. The mobile app economy is projected at $1.2 trillion. There are 4.69 billion smartphone users worldwide, each generating revenue for Big Tech through attention, data, and engagement. The compensation flowing back to those users: $0. Screen time has never declined year-over-year. The structural imbalance between who provides the attention and who captures the value is the defining economic asymmetry of the digital era — and the companies flipping this model are building revenue streams that operate outside the interest rate cycle, outside forced index rebalancing, and outside the macro pressures threatening traditional portfolios.

SpaceX changed how we reach the stars. Starlink changed how the world connects to the internet. But there is still one massive problem: the devices in our pockets are still “dumb.” Mode Mobile ($MODE) is bringing “EarnOS” to the world’s 7 billion smartphones — the first device designed to put money in your pocket by rewarding you for every song, game, and charge. With $115M in revenue and $11.8M as EBITDA and a growth rate of 32,481%, Deloitte just named them the #1 fastest-growing software company in North America. They’ve already reserved their Nasdaq ticker ($MODE) at $0.50 per share.

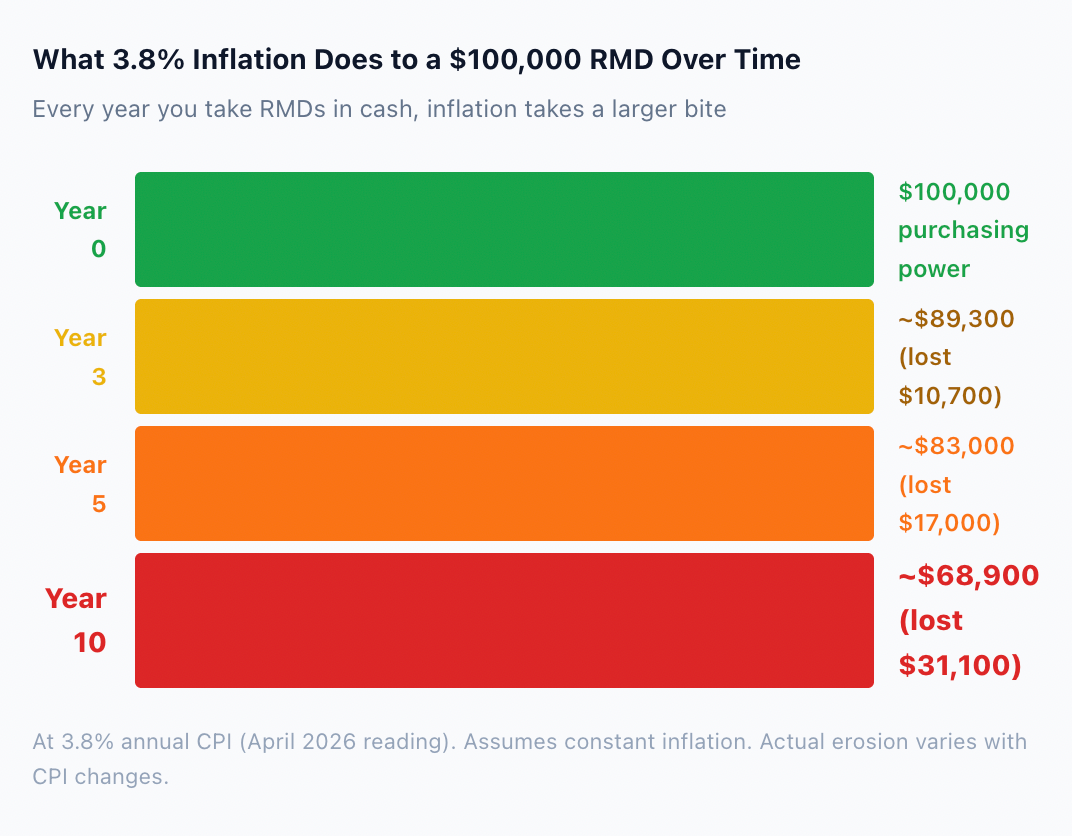

Meanwhile, if you’re near or over 73, your Required Minimum Distributions may be bleeding money. Most retirees take RMDs the default way — in cash. At 3.8% CPI, every cash dollar withdrawn buys less than when it was earned. Over 10 years at current inflation, a $100,000 distribution loses over $31,000 in purchasing power. What most retirees don’t realize is that IRS Code 408(m) allows RMDs to be handled differently — in a way that may help protect more of what you’ve earned. Once the distribution hits your account, options shrink fast. A free guide explains the #1 RMD trap and how some retirees are repositioning before it’s too late.

When your phone generates $390 billion for someone else and your RMD strategy quietly erodes your purchasing power at 3.8% per year, the cost of accepting the defaults is measurable and growing. The Americans who rejected both defaults — turning their phone from a cost center into an earning device, and turning their RMD from a cash drain into a protected allocation — are the ones whose wealth is compounding while the defaults erode everyone else’s. Both fixes are available right now. Both start with a free guide. And both become more valuable as inflation persists and the attention economy grows.