Your Bank Account Is About to Change — 4 Things You Need to Do Before It Does

4 Simple Steps to Protect Your Bank Account

The US government could make a sweeping change to bank accounts nationwide. Giving them unprecedented powers to control your bank account. They could closely track every transaction. They could even freeze it.

Fortunately, there are 4 simple steps you can take to safeguard your savings.

| Discover these 4 simple steps here → |

Right now, there are four separate government initiatives converging on your bank account. Each one, on its own, represents a significant expansion of federal power over your money. Together, they form a system of financial control that has no precedent in American history.

Most Americans are completely unaware of what is happening. The changes are being rolled out incrementally, buried in regulatory filings and policy dockets that are designed to avoid public attention. By the time the average person notices, the architecture will already be in place.

The good news is that there are still concrete steps you can take to protect your savings before these changes become fully operational. Discover these 4 simple steps here (AD).

The Four Threats to Your Bank Account

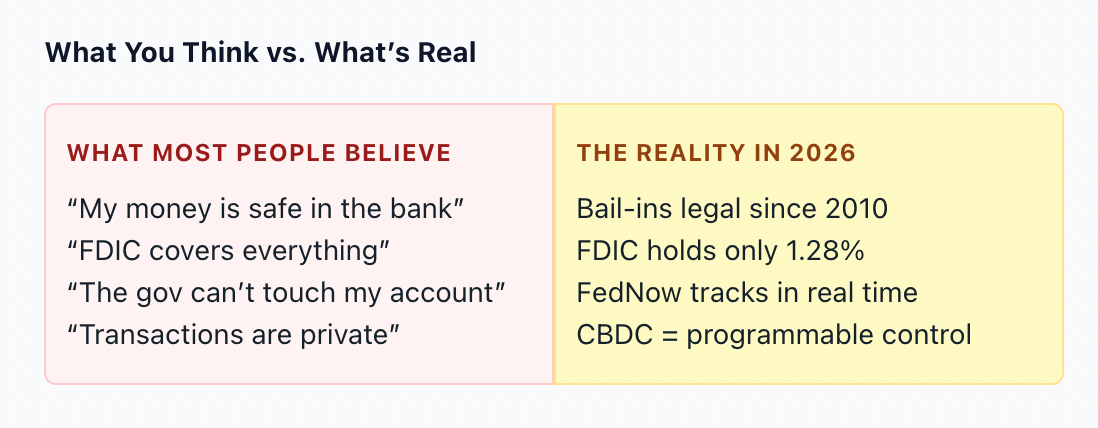

1. FedNow — Real-Time Transaction Surveillance. The Federal Reserve’s instant payment system is now operational 24/7/365. Unlike the old ACH batch system, FedNow creates a centralized, real-time digital trail of every transaction. Every transfer, bill payment, purchase, and donation is logged instantly through a single Federal Reserve hub. The buffer that once separated your transactions from government visibility no longer exists.

2. CBDC — Programmable Money. The Central Bank Digital Currency initiative would give the government the ability to issue digital dollars with built-in rules. Expiration dates on payments. Spending restrictions by category. Geographic limits on where your money works. Currency that the issuer can program is currency the issuer controls.

3. Bail-In Authority — Your Deposits Are Not Yours. Since 2010, U.S. banks have the legal right to use depositor funds to stabilize their own balance sheets during a crisis. When you deposit money into a bank, you are technically lending it to them. If the bank fails, your deposits can be seized to cover losses before you see a dime.

4. FDIC Fragility — The Safety Net Has Holes. FDIC insurance covers $250,000 per depositor, but the emergency reserve fund holds just 1.28% of total insured deposits. If multiple major banks failed simultaneously, the fund would be exhausted almost immediately. During a true crisis, payouts could take months or years.

This Has Already Happened — With Worse Tools

In Cyprus in 2013, the government confiscated up to 47.5% of uninsured bank deposits overnight. No warning. No vote. In Canada in 2022, bank accounts were frozen without court orders during the trucker protests. In Lebanon in 2019, depositors lost access to over $72 billion and faced $400 monthly withdrawal limits — some resorted to desperate measures just to access their own savings.

Every one of these events happened under legacy banking systems that were slower and less centralized than what the U.S. is building right now. FedNow, the CBDC, and the bail-in framework together create a system that makes Cyprus-style interventions not just possible but instantaneous. The friction that once slowed government action — batch processing, institutional pushback, logistical delays — has been engineered out of the system.

The people who protected their wealth in Cyprus and Canada were the ones who took action before the crisis hit. The ones who waited found the exits already closed. Discover these 4 simple steps here (AD).

$0.50/share for the #1 software company?

One of America’s fastest-growing software companies might surprise you🆘

Heads up! It’s not the publicly traded tech giant you might expect… Meet $MODE, the disruptor turning phones into potential income generators. Retail investors are buzzing about the company’s pre-IPO offering.

📲Mode saw 32,481% revenue growth over a three year period, ranking them the #1 overall software company on Deloitte’s 2023 fastest-growing companies list.

They aim to pioneer “Privatized Universal Basic Income” powered by technology—not government. Their flagship product, EarnPhone, turns phones from an expense into an income stream, and they’ve already helped consumers earn & save $1B+.

Uber did it to taxis, Airbnb to hotels and now Mode Mobile is doing it to the $500 billion smartphone industry. The difference? Early investors like you can invest in their pre-IPO offering at just $0.50/share and earn up to 20% bonus.

59,000+ shareholders already invested $71M+ and they may soon reach a point where they no longer accept outside investment.

🔒 With their Nasdaq ticker $MODE secured, investors now have a limited time to invest before they potentially go public.

| Early investors can earn up to 20% bonus shares → |

Please read the offering circular and related risks at invest.modemobile.com. This is a paid advertisement for Mode Mobile’s Regulation A+ Offering. Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur. The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period. Pro forma revenue and EBITDA, includes full year numbers of the businesses acquired throughout 2025.

Where the Smart Money Goes When Banks Get Risky

When the banking system comes under stress, capital flows toward two things: hard assets that cannot be frozen with a keystroke, and growth companies that operate outside the traditional financial grid.

On the hard asset side, physical gold and silver have been the default safe haven for thousands of years. They cannot be programmed, tracked, or remotely seized. They do not depend on a server staying online or a government choosing to honor its obligations. That is why demand for physical metals has hit multi-year highs — institutional and retail buyers alike are moving wealth outside the digital banking grid.

On the growth side, investors are looking at companies building the next generation of digital infrastructure — platforms that capture value from the massive shifts happening in how people work, earn, and interact with technology. The smartphone industry alone is worth $500 billion, and the companies disrupting it with new models of earning and ownership are attracting significant capital.

The Window Is Closing

Every one of these government initiatives — FedNow, CBDC, bail-in authority — is moving forward regardless of which party is in power. The infrastructure is being built. The legal framework is in place. The only variable is timing, and the clock is running.

The Americans who will weather what is coming are the ones who took steps to protect their savings while they still had the option. History has shown that by the time the crisis arrives, the exits are already closed. Discover these 4 simple steps here (AD).

Share this with someone who still assumes their bank account is untouchable. The legal framework says otherwise.