Trump’s $2,000 Tariff Dividend, the Supreme Court Deadline, and the Bank Branches Disappearing Across America

Trump’s Secret Loophole Could Save Your 401(k)—Act Now!

Trump has proposed to send $1,000–$2,000 checks directly to Americans — not as a bailout, but as a tariff dividend.

In Trump’s own words: “This is a dividend for the American people.”

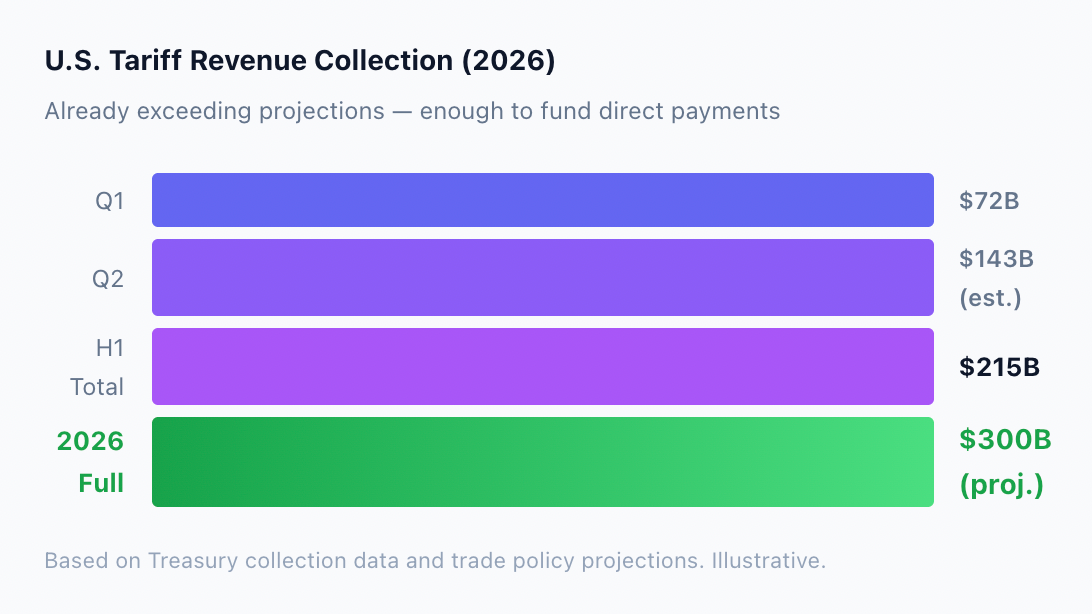

Already, more than $215 BILLION has been collected from tariffs in 2026, with projections reaching $300 BILLION by year’s end. Trump’s plan would redirect this money away from Washington bureaucrats and straight into the pockets of ordinary Americans.

But here’s the catch: the Supreme Court could BLOCK this plan in November — stripping you of a potential $2,000 check.

That’s why waiting is dangerous. You can’t rely on Washington to secure your future. While politicians bicker, inflation grows and retirement accounts take the hit.

Inside the FREE Wealth Protection Guide, you’ll discover how to:

• Safeguard your 401(k), IRA, or TSP from government overreach.

• Use IRS rules that allow eligible rollovers to shield savings with gold, tax-free and penalty-free.

• Protect your money no matter what the Supreme Court decides.

| Click Here Now to Claim Your FREE Wealth Protection Guide → |

There are two stories colliding in America right now that will affect every person with a bank account, a retirement plan, or a mailbox. One story is about money flowing in. The other is about money becoming harder to access. And most people are only paying attention to one of them.

The first story: the White House has proposed sending $1,000 to $2,000 checks directly to Americans — funded entirely by tariff revenue, not debt. Over $215 billion has already been collected in 2026, with projections approaching $300 billion by year’s end. The plan would redirect that money away from Washington and into the pockets of ordinary citizens.

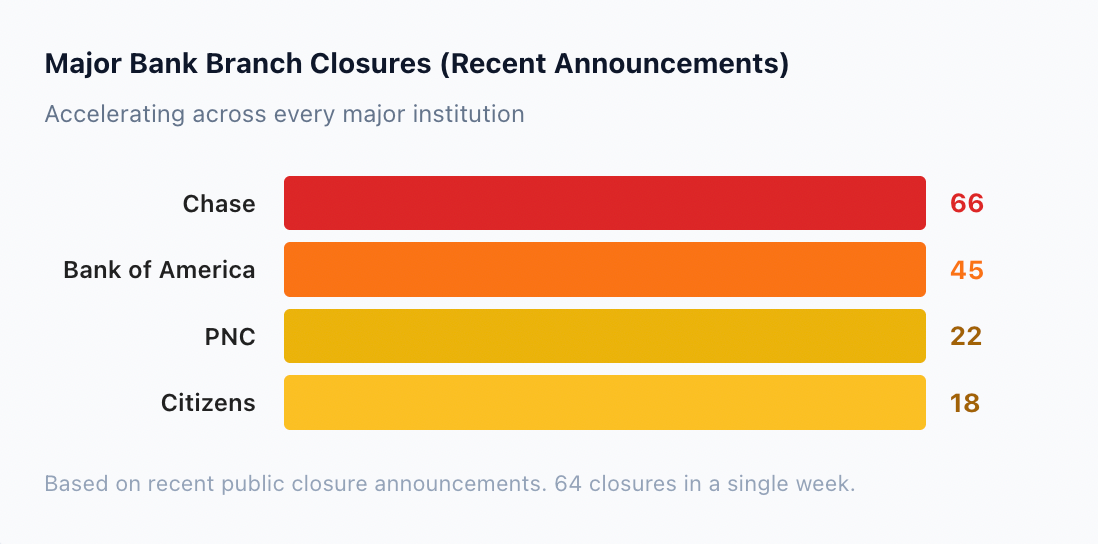

The second story: bank branches are closing at a pace that is accelerating month by month. PNC, JPMorgan Chase, Citizens Bank, Bank of America — major institutions are quietly shuttering locations across the country. In a single recent week, 64 closures were announced.

These two trends are not unrelated. They are both symptoms of a financial system in transition — and the Americans who understand what is driving both will be far better positioned than those who are blindsided by either.

The Tariff Dividend: What It Is and Why It Could Disappear

The concept is simple. The United States is collecting hundreds of billions of dollars in tariff revenue from foreign imports. Rather than letting that money disappear into the federal budget, the proposal is to distribute a portion of it directly to American citizens as a dividend.

In the President’s own words: “This is a dividend for the American people.” The amounts being discussed range from $1,000 to $2,000 per person. It is not structured as a bailout or a stimulus check. It is framed as a return on a national trade policy — money that was collected from foreign companies and redirected to domestic citizens.

The numbers are real. The revenue is being collected. But there is a critical deadline that most Americans do not know about: the Supreme Court is expected to rule on the constitutionality of the tariff dividend program in November. If the court blocks it, the checks stop. The money stays in Washington. And the window closes permanently.

This is why the conversation cannot be just about the dividend itself. It has to be about what happens to your financial position regardless of what the court decides. Relying on a potential $2,000 check to shore up your retirement is not a strategy. Having a plan that works whether the check arrives or not — that is a strategy.

Your 401(k) Is More Exposed Than You Think

The tariff dividend conversation has exposed a deeper vulnerability that affects millions of Americans: traditional retirement accounts are far more susceptible to government policy shifts than most people realize.

Your 401(k), IRA, or TSP is governed by a web of tax rules, withdrawal requirements, and regulatory frameworks that Congress can change at any time. The contribution limits, the tax treatment, the age at which you can access your own money without penalty — all of it is policy, and policy changes with every administration.

Meanwhile, inflation has been quietly eroding the purchasing power of every dollar sitting in those accounts. The cost of groceries, insurance, housing, and healthcare has risen faster than the official numbers suggest. Your account balance may look the same. But what it buys is shrinking year by year.

The Americans who are thinking clearly about this are not waiting for the dividend check. They are securing their retirement accounts now. Trump has proposed to send $1,000–$2,000 checks directly to Americans — not as a bailout, but as a tariff dividend. In Trump’s own words: “This is a dividend for the American people.” Already, more than $215 BILLION has been collected from tariffs in 2026, with projections reaching $300 BILLION by year’s end. But here’s the catch: the Supreme Court could BLOCK this plan in November — stripping you of a potential $2,000 check. That’s why waiting is dangerous. You can’t rely on Washington to secure your future. While politicians bicker, inflation grows and retirement accounts take the hit.

Click here now to claim your FREE Wealth Protection Guide and lock in control over your financial future today (AD).

Your Bank Branch Next to Close

Your Bank Branch Next to Close??? Why are bank branches quickly and quietly closing across the country?? Click here to see why — and see how to protect your accounts while there is still time.

• PNC Bank: 22 Branches Closing.

• JP Morgan Chase: 66 Branches Closing.

• Citizens Bank: 18 Branches Closing.

• Bank of America: 45 Branches Closing.

In just one week recently, 64 bank branch closures were announced. What’s going on? And is your bank branch next?

| Click here now to see the details → |

Meanwhile, Your Local Bank Branch Is Disappearing

While Washington debates tariff dividends and the Supreme Court prepares its ruling, something is happening at street level that most Americans are not paying attention to until it affects them directly: bank branches are closing at an accelerating rate across the country.

This is not a gradual consolidation. It is a rapid restructuring of how Americans access their own money. The closures are concentrated in communities that can least afford to lose them — rural areas, small towns, and older neighborhoods where residents depend on in-person banking for everything from depositing checks to resolving account issues.

The scale is staggering. Why are bank branches quickly and quietly closing across the country? PNC Bank: 22 Branches Closing. JP Morgan Chase: 66 Branches Closing. Citizens Bank: 18 Branches Closing. Bank of America: 45 Branches Closing. In just one week recently, 64 bank branch closures were announced. What’s going on? And is your bank branch next?

Click here now to see the details (AD).

What the Branch Closures Actually Signal

Banks do not close profitable branches. They close branches when the cost of maintaining a physical presence exceeds the revenue it generates — or when the institution is preparing for a structural shift in how it delivers services.

The shift underway is the same one driving the FedNow rollout and the CBDC development: the transition from physical, in-person banking to a fully digital, centrally controlled financial system. Every branch that closes is one more step toward a world where your relationship with your money is mediated entirely through screens, servers, and systems you do not control.

When your bank had a branch on Main Street, you could walk in, talk to a person, and access your money in real time. When that branch closes and your banking moves entirely online, you are dependent on the bank’s servers staying up, its policies remaining favorable, and its compliance department not flagging your account for any reason. The friction that once protected you — the human element, the face-to-face relationship — is being removed.

The Convergence: Tariffs, Branches, and Your Retirement

These three trends — the tariff dividend, the branch closures, and the retirement account vulnerability — are converging into a single picture that every American needs to understand.

The tariff dividend offers a short-term cash injection that may or may not survive the Supreme Court. The branch closures signal a long-term transition toward a banking system that is less accessible and more controlled. And your retirement accounts sit in the middle — subject to both the policy shifts in Washington and the structural changes in how banks operate.

The people who navigate this successfully are the ones who take a multi-layered approach: secure their retirement accounts against government overreach now, understand how their banking access is changing, and position their wealth so that no single policy decision or institutional failure can put it at risk.

The tools to do this already exist within the tax code. Inside the FREE Wealth Protection Guide, you’ll discover how to: Safeguard your 401(k), IRA, or TSP from government overreach. Use IRS rules that allow eligible rollovers to shield savings with gold, tax-free and penalty-free. Protect your money no matter what the Supreme Court decides.

Click here now to claim your FREE Wealth Protection Guide and lock in control over your financial future today (AD).

The Quiet Transition to a System You Do Not Control

The branch closures are not happening in isolation. They are part of a broader transition toward a financial system where every transaction is digital, every account is centralized, and every dollar is trackable in real time. FedNow is already operational. The CBDC framework is being built on top of it. And every branch that closes pushes another community into a system where the only way to access your money is through digital channels that the government can monitor and, if it chooses, control.

The precedents are clear. Cyprus confiscated deposits. Canada froze accounts. Lebanon locked depositors out of their own savings. Every one of those events happened in systems that were less centralized and less digital than what the U.S. is building right now.

Three Threats. One Window to Act.

The tariff dividend may arrive — or the Supreme Court may kill it. Your local bank branch may stay open — or it may be on next month’s closure list. Your retirement account may hold its value — or inflation and policy changes may erode it year by year.

The one thing that is certain is that the financial landscape is shifting faster than it has in decades, and the Americans who prepare while the window is open will be in a fundamentally different position than those who wait and react.