Trump Promised $2,000 Rebate Checks. The Math Says There Isn’t Enough Money. Unless Washington Plays the Gold Card.

Trump’s Rebate Stimulus Just Dropped — Are You Ready?

Donald Trump just did it again. At a rally, he confirmed his Rebate Stimulus Plan — but it’s not just about sending out checks.

Behind closed doors, Trump’s team is pushing a strategic wealth-protection move that could matter far more than a one-time payment.

Why now?

✅ Skyrocketing inflation

✅ A weakening dollar

✅ Markets spinning out

This isn’t just a “bonus” — it’s a chance to shield your savings from what’s coming.

And while Washington hands out checks, the people who act before the next wave hits could be the only ones who come out ahead.

Get your FREE 2026 Gold Protection Guide now. It’s fast, no cost, and could be the smartest move you make this year.

P.S. Once those checks start rolling out, this window may slam shut.

| 👉 Claim My FREE Guide |

Trump promised $2,000 rebate checks for working-class American families. Late last year, he made a series of Truth Social posts backing the plan, and economic advisor Kevin Hassett told CBS that “in the new year, the president will bring forth a proposal to Congress to make that happen.” Democrats responded with their own bill — Senator Martin Heinrich introduced legislation offering $1,200 to joint filers under $180,000, plus $600 per dependent. Both parties want credit for putting money in Americans’ pockets before the 2026 midterms.

But the math does not work. Fortune calculated that even paying $2,000 per household to just the bottom 50% of earners would require $135 billion — nearly half of all tariff revenue collected in 2025. The Senate Joint Economic Committee estimates households already paid $1,725 in tariff costs on average between February 2025 and January 2026. As one certified financial planner told CNBC: “There does not appear to be sufficient political support to move such a measure through Congress.” The checks are popular. The funding is not there.

Meanwhile, the context in which those checks would arrive makes the situation worse, not better. Inflation is still above the Fed’s 2% target. Companies are projecting price increases above 3% in 2026. The Fed kept rates unchanged in April. Economists warn that injecting new stimulus while inflation pressures are rising “would be risky.” The rebate checks are designed to offset tariff costs — but they could amplify the very inflation they are meant to address.

The Americans who understand this dynamic are not waiting for checks. They are positioning their savings now.

Donald Trump just did it again. At a rally, he confirmed his Rebate Stimulus Plan — but it’s not just about sending out checks. Behind closed doors, Trump’s team is pushing a strategic wealth-protection move that could matter far more than a one-time payment. Why now? Skyrocketing inflation. A weakening dollar. Markets spinning out. This isn’t just a “bonus” — it’s a chance to shield your savings from what’s coming. And while Washington hands out checks, the people who act before the next wave hits could be the only ones who come out ahead. Claim My FREE Guide (AD).

$39 Trillion in Debt. $1 Trillion in Annual Interest. Zero Political Will to Fix It.

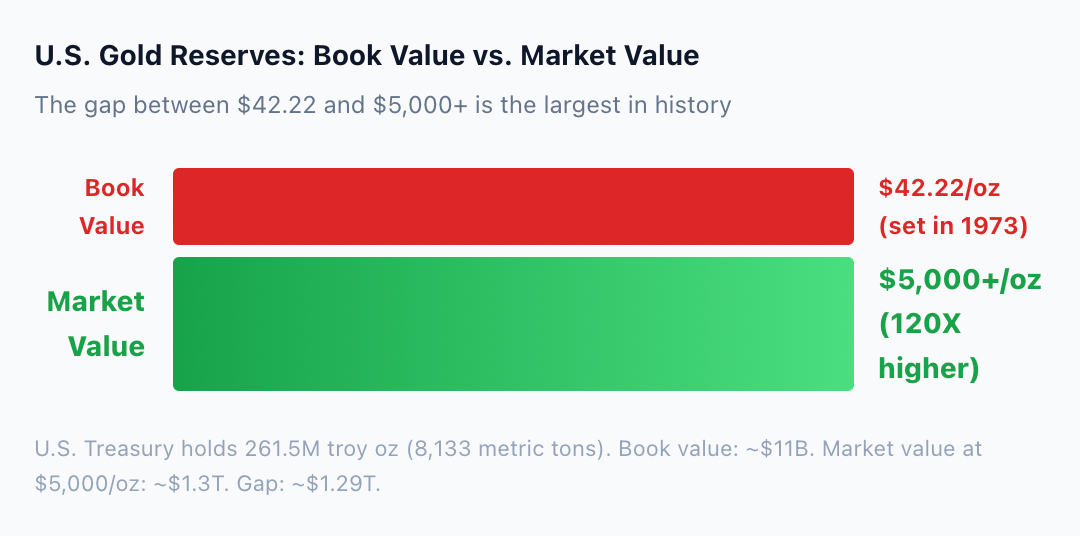

The U.S. holds 261.5 million troy ounces of gold — the largest official gold reserve in the world. It sits in Fort Knox, West Point, and the Denver Mint. On the government’s books, that gold is valued at $42.22 per ounce — a price set in 1973 and never updated. At today’s market price above $5,000 per ounce, the reserve is worth over $1.3 trillion. The difference between the book value (~$11 billion) and the market value (~$1.3 trillion) is approximately $1.29 trillion — sitting on the balance sheet as unrealized value that the government has never officially acknowledged.

The “Nuclear Option” That Requires No Vote, No New Taxes, and No Warning

In August 2025, the Federal Reserve published a research note titled “Official Reserve Revaluations: The International Experience,” documenting how five countries — Germany, Italy, Lebanon, Curacao and Saint Martin, and South Africa — monetized their gold reserves to raise funds without selling a single ounce. The process is an accounting exercise: retire old gold certificates and issue new ones at a higher price. The difference becomes a cash infusion for the government. No new taxes. No new debt. No vote in Congress.

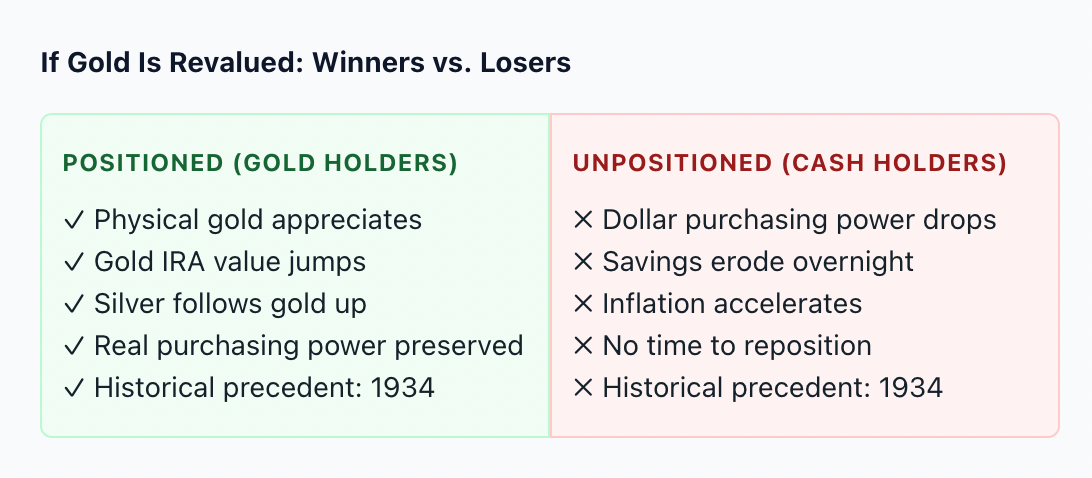

Treasury Secretary Scott Bessent set off speculation in February when he said: “Over the next 12 months, we will monetise the assets listed in the federal budget and extract value from them.” He later clarified that he “didn’t mean repricing gold.” But the Fed’s own accounting guidance confirmed that the Secretary of the Treasury has the legal authority to issue gold certificates at any price. And the historical precedent is clear: in 1934, FDR repriced gold from $20.67 to $35 per ounce with one executive order — devaluing the dollar 69% overnight and triggering the largest wealth transfer in modern history.

Bank of America’s head of commodities Francisco Blanch told Bloomberg that repricing gold would be “bullish for the gold market because it would show that gold is no longer this barbarous relic.” Analysts project that if gold were formally revalued, market prices could reach $10,000-$20,000 per ounce in a post-revaluation environment. The chain reaction would touch every dollar, every account, and every retirement fund in the country. By the time it makes headlines, the window to position is already shut.

EXPOSED: Washington Has One Drastic Move Left — No Vote Required

The U.S. debt just slammed through $39 trillion. Interest payments alone: $1 trillion this year. That’s $7,700 per household. Not to build roads. Not to fund schools. Just to cover Washington’s tab from years of running the printing press.

There is one move that closes this gap overnight. No new taxes. No new debt. No vote in Congress. No warning to you.

When the government owes $1 trillion a year just in interest — how long before they reach for the only tool that’s ever actually worked?

In 1934, FDR repriced gold with one executive order. Books changed overnight. Those who were positioned ended up on the right side of the largest wealth transfer in modern history. Those who weren’t — lost quietly and permanently.

America’s gold sits at $42.22 on the books. Market price is 120 times that. One signature closes the gap. The chain reaction touches every dollar, every account, every retirement fund you own.

By the time this makes headlines — the window is already shut.

What’s coming. How it works. Exactly how to position right now. All of it laid out free in this confidential report.

Once the move is made — you’re reacting. And reacting is always too late.

| → Access The Full Report Free — 30 Seconds To Request → |

What a Gold Revaluation Actually Does to Your Savings, Your Dollar, and Your Retirement

If the government reprices gold from $42.22 to market value, the immediate effect is a $1.29 trillion cash infusion to the Treasury — created from nothing more than changing a number on a ledger. That is not free money. It is a devaluation event. The dollar loses purchasing power proportional to the amount of new liquidity entering the system. Critics call it “backdoor money printing” because it increases the money supply without any Congressional authorization.

The 1934 precedent is instructive. FDR’s gold repricing increased the Treasury’s gold-backed wealth by 69%. But it also devalued the dollar by 41% relative to gold. Americans who held physical gold before the order were on the right side of the transfer. Americans who held only dollars lost purchasing power quietly and permanently. The same dynamic would apply today — but at a much larger scale, because the gap between the book value ($42.22) and the market value ($5,000+) is 120x, far wider than the 1934 gap.

You Already Owe More Than You Were Ever Told

The U.S. debt just slammed through $39 trillion. America’s gold sits at $42.22 on the books. Market price is 120 times that. In 1934, FDR repriced gold with one executive order — triggering the largest wealth transfer in modern history. One signature closes the gap today.

The Rebate Checks Are Coming. The Question Is What They’ll Be Worth When They Arrive.

The $2,000 rebate checks may or may not pass Congress. The $39 trillion debt is not going away. The $1 trillion in annual interest is not going away. And the 120x gap between the government’s gold book value and the market price is the largest in history. Something has to give. Whether it is a formal revaluation, an inflationary spiral, or a gradual debasement of the dollar, the outcome is the same for people who hold only cash: their purchasing power erodes. The people who hold tangible assets — gold, silver, real property — are positioned on the right side of whatever comes next.

The rebate checks are the headline. The gold revaluation is the story underneath. And while Washington hands out checks, the people who act before the next wave hits could be the only ones who come out ahead. Get your FREE 2026 Gold Protection Guide now. It’s fast, no cost, and could be the smartest move you make this year. P.S. Once those checks start rolling out, this window may slam shut. Claim My FREE Guide (AD).