The RMD Trap Is Draining Retirement Accounts — While the Digital Dollar Threatens What’s Left

The #1 RMD Trap for Retirees REVEALED

If you’re preparing to take Required Minimum Distributions (RMDs) in retirement, you need to read this:

Most retirees take their RMDs in cash, which seems logical... Until you realize what’s really happening: Every dollar you’re forced to withdraw could get hit immediately with income tax and advisor fees... Then it sits in a bank account, a sitting duck for inflation.

So, your nest egg has 3 beaks poking at it:

• Uncle Sam...

• Advisor commissions...

• And the “silent tax” of inflation...

Don’t let your account shrink faster than it needs to... Find out more on the next page 👉 How to Avoid the #1 RMD Trap

Here’s what is often overlooked: The IRS Code 408(m) lets you take RMDs differently by moving them into tangible physical assets like precious metals. Legally, the same RMD requirement can be met... But you could help protect your savings with trusted legacy assets like gold and silver — instead of leaving them more vulnerable to taxes, fees, inflation, and economic storms.

You need to see this hidden strategy: 👉 Tap HERE to Discover How Americans Are Protecting Their Savings in 2026 (Plus, Request Your Free Wealth Protection Guide)

It’s time to find out how thousands are using gold & silver to help shield what they’ve spent decades building through hard work. Precious metals’ record-breaking run has spilled into 2026 as gold recently eclipsed $5,600 and silver hit $119... And just as they have for thousands of years, they could be well-positioned to continue helping protect accounts in these uncertain times.

| Find out more about this RMD strategy now → |

Allegiance Gold, LLC is not a broker-dealer and does not provide investment, tax, or legal advisory services. Precious metals, like all investments, carry risk, are not suitable for all investors, and past performance does not guarantee future results. Please consult your own investment, tax, or legal advisor prior to making any investment decision. ©Allegiance Gold, LLC 2026

Two threats are converging on American retirement accounts right now — and most retirees are aware of neither. The first is structural: the Required Minimum Distribution system is designed to force you to withdraw money from your retirement accounts every year starting at age 73, whether you need the money or not. The second is systemic: the U.S. government is building the infrastructure for a Central Bank Digital Currency that would give Washington unprecedented control over every dollar in the financial system.

Each of these threats is serious on its own. Together, they create a scenario where your retirement savings are simultaneously being drained from within (by taxes, fees, and inflation on forced RMD withdrawals) and threatened from without (by a digital surveillance currency that could monitor, limit, or freeze your assets without a court order).

But there is a legal mechanism — buried in IRS Code 408(m) — that addresses both threats simultaneously. And most financial advisors have never mentioned it to their clients.

The retirees who understand this mechanism are repositioning right now, while it is still available. If you’re preparing to take Required Minimum Distributions (RMDs) in retirement, you need to read this: Most retirees take their RMDs in cash, which seems logical... Until you realize what’s really happening: Every dollar you’re forced to withdraw could get hit immediately with income tax and advisor fees... Then it sits in a bank account, a sitting duck for inflation. So, your nest egg has 3 beaks poking at it: Uncle Sam... Advisor commissions... And the “silent tax” of inflation... Here’s what is often overlooked: The IRS Code 408(m) lets you take RMDs differently by moving them into tangible physical assets like precious metals. Find out more about this RMD strategy now (AD).

How RMDs Quietly Destroy Wealth in Three Steps

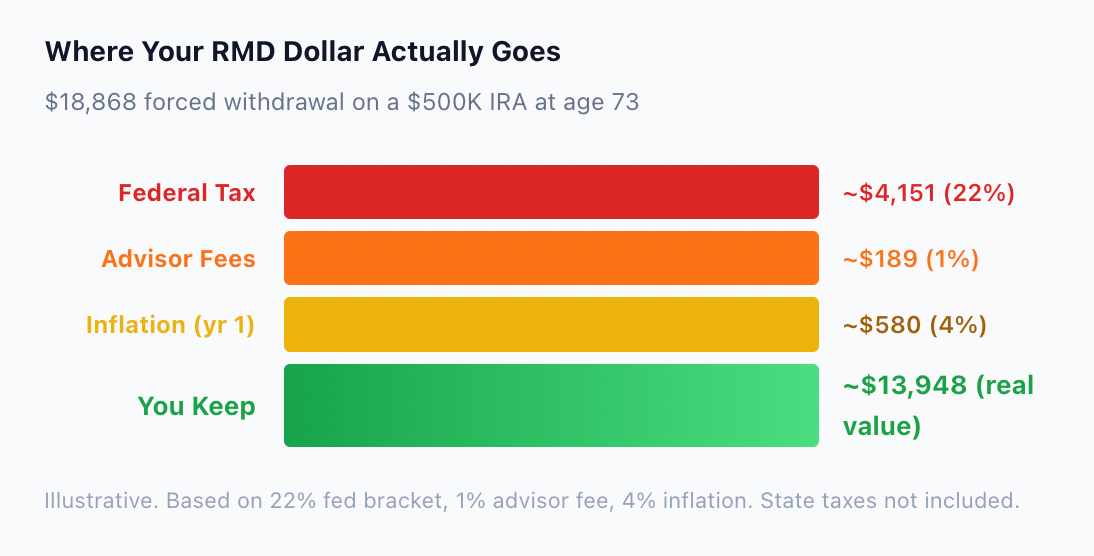

The RMD system sounds simple: once you turn 73, you must withdraw a minimum amount from your tax-deferred retirement accounts each year. Miss the deadline, and the IRS hits you with a 25% penalty on the amount not withdrawn. But the real cost is not the penalty. It is what happens to the money you are forced to take out.

|

🚨 The RMD Wealth Drain: 3 Steps Step 1: Forced withdrawal. The IRS mandates you pull money out of your account whether you need it or not. A $500,000 IRA at age 73 forces a $18,868 withdrawal. Step 2: Immediate taxation. The full withdrawal is taxed as ordinary income. At a 22% bracket, that is $4,151 gone instantly — before you touch a dollar. Step 3: Inflation erosion. The remaining cash sits in a bank account earning 0.5% interest while inflation runs at 3-4%. Each year, the purchasing power of that withdrawal shrinks. In 10 years, it buys 30% less. |

IRS Code 408(m): The RMD Strategy Most Advisors Never Mention

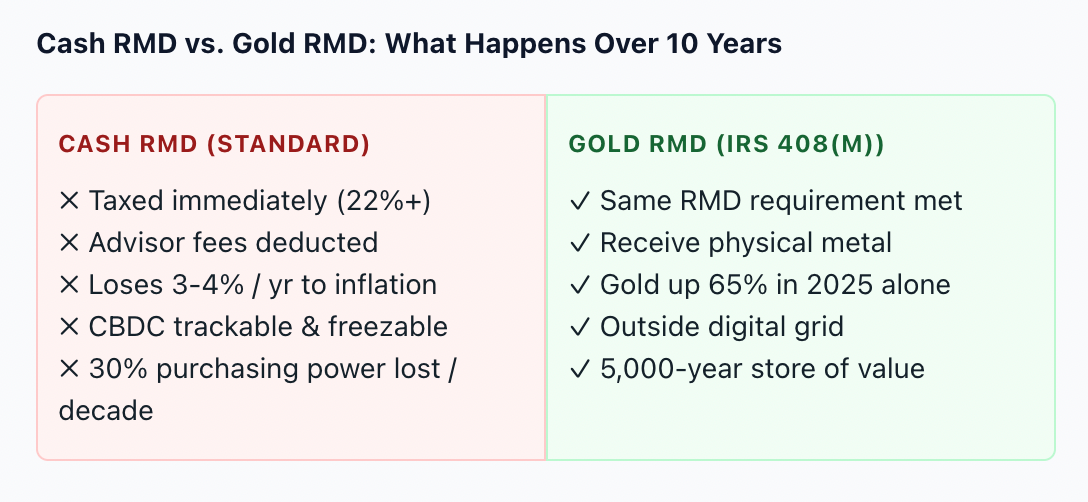

Most financial advisors present RMDs as a cash-only event: withdraw dollars, pay taxes, deposit what is left into a taxable account. But the IRS code does not require cash withdrawals. IRS Code 408(m) explicitly permits certain physical assets — including gold, silver, platinum, and palladium meeting specific purity standards — to be held inside self-directed IRAs.

This means you can take your RMD “in kind” — receiving physical precious metals instead of cash. The RMD requirement is still met. The taxes are still owed on the fair market value. But instead of cash sitting in a bank account losing purchasing power every month, you now hold a tangible asset that has appreciated 65% in the past year alone and has maintained purchasing power for over 5,000 years.

The difference in outcomes over a 10-year retirement horizon is dramatic. Cash RMDs depreciate every year. Gold RMDs have historically appreciated — particularly during the inflationary and geopolitically uncertain environments that define the current era. The IRS allows it. The mechanism exists. The question is whether your advisor has told you about it.

|

📰 Related Reading • IRS.gov: RMDs begin at age 73 under SECURE 2.0; 25% penalty for missed distributions • Fortune (Apr 22, 2026): Gold at $4,746/oz, up 25%+ since early 2025, driven by inflation and uncertainty • J.P. Morgan Research: Forecasts gold to average $5,055/oz by Q4 2026 and $5,400/oz by end of 2027 • Kiplinger (Mar 2026): Gold hit $5,500/oz after gaining 65% in the historic 2025 rally • U.S. House (Jul 2025): Anti-CBDC Surveillance State Act passed 219-210, codifying Trump’s CBDC ban |

The Second Threat: The Digital Dollar and the End of Financial Privacy

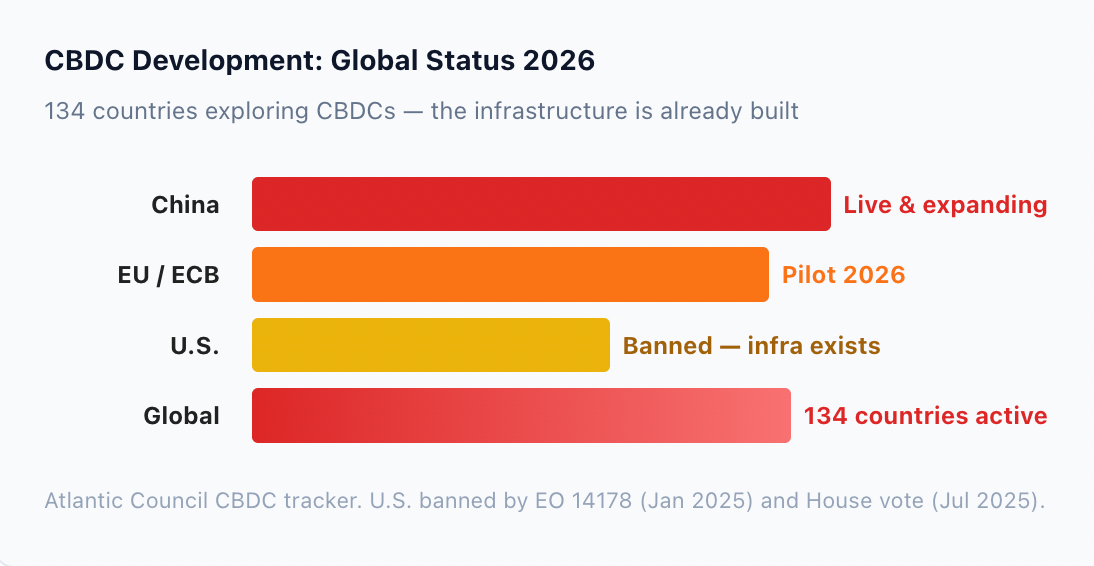

While the RMD system drains your account from within, a second threat is building from the outside. The U.S. government has been developing the infrastructure for a Central Bank Digital Currency — a programmable digital dollar that would give Washington real-time visibility into every transaction, the ability to impose limits on spending or cash holdings, and the technical capacity to freeze assets without judicial review.

Trump signed Executive Order 14178 in January 2025, prohibiting federal agencies from establishing or promoting a CBDC. The House passed the Anti-CBDC Surveillance State Act in July 2025 by a vote of 219-210. But the infrastructure that was built under the previous administration — including FedNow’s real-time settlement system — remains in place. The rails for a digital dollar exist. Whether they are activated depends on who holds power next.

The pattern from other countries is clear. China’s digital yuan already monitors and restricts spending. In pilot programs, digital currency was programmed to expire — forcing citizens to spend their savings on the government’s timeline. As Congressman Tom Emmer warned: “If not designed to be open, permissionless, and private, a government-issued CBDC is nothing more than an Orwellian surveillance tool.” The U.S. has banned it for now. But bans can be reversed. And the infrastructure is already in place.

Trump’s Currency “Nuclear Option”

There’s a quiet countdown happening. Once it hits zero, every dollar you own could be monitored. And most Americans don’t even see it coming.

The U.S. government is moving forward with its CBDC program. When it’s active, they’ll have full control over your money. They will know what you buy, how much you spend, and even when. Every transaction you make will be tracked.

This may be your final chance to legally “opt out” before the Digital Dollar becomes mandatory.

Our confidential new guide explains how to protect your cash, privacy, and freedom. But it may not stay online for long. Don’t wait because every day you delay gives them more control.

| 👉 Claim Your FREE Digital Dollar Protection Guide Now |

Why Physical Gold Solves Both Problems Simultaneously

Physical gold held inside a self-directed IRA addresses the RMD trap because it converts forced withdrawals from a depreciating asset (cash) into an appreciating one (precious metals). It addresses the CBDC threat because physical gold sits outside the digital surveillance grid entirely — a government cannot freeze, track, or program an asset that exists as a tangible object in your possession.

Central banks understand this. They have been net buyers of gold for over 15 consecutive years, accumulating over 1,000 tonnes per year since 2022. J.P. Morgan projects approximately 755 tonnes of central bank purchases in 2026. They are converting dollar reserves into physical gold because they see the same threats that individual retirees are facing — and they are acting on it.

Most Americans Have No Idea What’s Coming

There’s a quiet countdown happening. Once it hits zero, every dollar you own could be monitored. The U.S. government is moving forward with its CBDC program. When it’s active, they’ll have full control over your money.

This may be your final chance to legally “opt out” before the Digital Dollar becomes mandatory.

Two Threats. One Solution. One Window.

The RMD system will continue draining your account every year. The digital dollar infrastructure will continue being built. The only variable is whether you reposition a portion of your savings into an asset that is immune to both — while the legal mechanism to do so (IRS Code 408(m)) and the political window (Trump’s CBDC ban) are both still in effect.