The IRS Rule Most Americans Have Never Heard Of Could Protect Your 401(k) from What’s Coming. And a 0% APR Window Just Opened.

IRS 408(m) Exposed

Did you know there’s an IRS rule — 408(m) — that may allow certain retirement savers to move part of a 401(k), IRA, TSP, or 403(b) into physical gold and silver… without triggering early-withdrawal penalties and while keeping retirement tax advantages intact?

Most Americans have never even heard of it.

Yet wealthy investors use strategies like this to protect gains, reduce exposure, and stay positioned when markets turn violent.

It’s a legal, IRS-recognized framework — one that can help you protect retirement wealth without selling everything into cash. We broke it down step-by-step in a FREE 408(m) guide.

| 👉 Grab your FREE 408(m) Guide Now |

Allegiance Gold, LLC is not a broker-dealer and does not provide investment, tax, or legal advisory services. No statement in this communication should be construed as a recommendation to purchase or sell any security, or as investment, tax, or legal advice. Precious metals, like all investments, carry risk, are not suitable for all investors, and past performance does not guarantee future results. We do not guarantee any investment performance. Please consult your own investment, tax, or legal advisor prior to making any investment decision. Third-party information quoted or presented by us in this communication represents only the opinions of the third party and we do not endorse any third-party source of information. We are not affiliated with the U.S. Mint or any government agency. Copyright Allegiance Gold, LLC 2026

IRS Section 408(m) is one of the least-discussed provisions in the Internal Revenue Code — and one of the most consequential for retirement savers in 2026. The rule defines which physical assets can be held inside a self-directed IRA, including specific types of gold, silver, platinum, and palladium coins and bars that meet minimum fineness requirements. When used correctly through a direct trustee-to-trustee transfer, it allows retirement savers to move part of a 401(k), traditional IRA, TSP, or 403(b) into physical precious metals without triggering early-withdrawal penalties and while maintaining the tax-deferred status of the account.

The timing of this rule’s relevance could not be more critical. The Fed just held rates at 3.5-3.75% in an 8-4 split vote — the most fractured FOMC decision since 1992. Gold sits at $4,885 per ounce. The SpaceX IPO is about to trigger $33-52 billion in forced portfolio rebalancing. The Iran war has sent energy prices surging. And the U.S. national debt stands at $39 trillion with $1 trillion in annual interest payments. Traditional retirement portfolios — built on stocks and bonds — are facing simultaneous pressure from inflation, geopolitical risk, and forced index rebalancing. Physical gold held inside a tax-advantaged retirement account is the only allocation that sits entirely outside all three of those pressures.

For 2026, the IRA contribution limit is $7,500, with a “super catch-up” of $8,600 for investors aged 60-63 — the highest catch-up contribution in IRA history. This four-year window, created by the SECURE 2.0 Act, was specifically designed to help near-retirement savers strengthen their positions. The Americans who understand Section 408(m) are using that window to diversify a portion of their retirement savings into physical gold and silver — without triggering taxes, penalties, or selling into cash.

The wealthy have used this strategy for decades. Most Americans have never heard of it.

Did you know there’s an IRS rule — 408(m) — that may allow certain retirement savers to move part of a 401(k), IRA, TSP, or 403(b) into physical gold and silver… without triggering early-withdrawal penalties and while keeping retirement tax advantages intact? Yet wealthy investors use strategies like this to protect gains, reduce exposure, and stay positioned when markets turn violent. It’s a legal, IRS-recognized framework — one that can help you protect retirement wealth without selling everything into cash. We broke it down step-by-step in a FREE 408(m) guide. Grab your FREE 408(m) Guide now (AD).

Why 2026 Is the Most Dangerous Year for Traditional Retirement Portfolios Since 2008

The Americans using Section 408(m) are not abandoning their retirement accounts. They are diversifying a portion — typically 5-20% — into physical gold and silver held inside the same tax-advantaged structure. The process is a direct trustee-to-trustee transfer with no taxable event, no early-withdrawal penalty, and no disruption to the existing account. The gold sits in an IRS-approved depository. The tax advantages remain intact. And the allocation provides genuine non-correlation — an asset whose value derives from scarcity and universal recognition rather than earnings multiples, interest rate policy, or currency stability.

While You Protect Your 401(k), Your Credit Card Debt Is Quietly Eating Your Present

The average American carries over $6,700 in credit card debt at an average APR of 22.76% — the highest rate in recorded history. Total U.S. credit card debt crossed $1.2 trillion in early 2026. Delinquency rates for credit cards have risen for 11 consecutive quarters. And the Fed’s decision to hold rates at 3.5-3.75% means those interest rates are not coming down anytime soon.

The math is punishing: at 22.76% APR, a $6,700 balance costs $1,524 per year in interest alone. That is $127 per month that goes to the credit card company, not your balance. Over three years, you would pay $4,573 in interest on a $6,700 balance — paying nearly 70% of the original amount in interest charges. The Americans who understand this are using a simple tool: 0% introductory APR balance transfer cards that eliminate interest for 15-21 months. Every payment goes toward the actual balance, not the bank’s profit margin.

The connection between retirement protection and credit card debt elimination is strategic: every dollar you save on credit card interest is a dollar that can be redirected toward building wealth. If you are paying 22.76% on credit card debt while simultaneously trying to protect your 401(k), you are fighting a war on two fronts. The smartest financial move in 2026 is doing both simultaneously: using Section 408(m) to diversify your retirement savings into physical gold, and using a 0% intro APR card to eliminate credit card interest while the window exists.

(0% intro APR until 2027)

Are you still paying 20% (or more) interest on your credit cards?

The average American carries over $6,700 in credit card debt —and some of it is just because of high interest.

But there’s a smarter move: Switch to a 0% intro APR card and pay no interest until 2027. That means your payment goes toward your balance—not high interest.

Here are some of the best offers available right now.

| See top 0% interest credit cards now → |

This is an advertisement.

This email contains references to products from one or more of our advertisers. FinanceBuzz is an informational website that provides tips, advice, and recommendations to help you make financial decisions. We strive to provide up-to-date information, but make no warranties regarding the accuracy of our information.

Ultimately, you are responsible for your financial decisions. FinanceBuzz is not a financial institution and does not provide credit cards or any other financial products. FinanceBuzz does not make any credit decisions. We may receive compensation from the products and services mentioned in this email.

Please click here to opt out of future emails from FinanceBuzz. 111 E. Atlantic Ave., Suite 200 Delray Beach, FL 33444

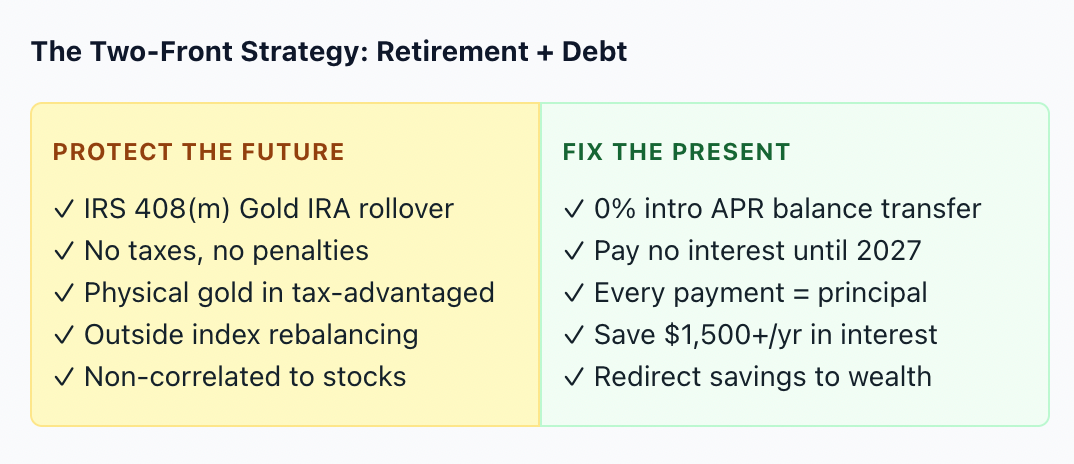

Protect the Future and Fix the Present: The Two-Front Financial Strategy for 2026

The Americans who are strongest financially in 2026 are the ones addressing both sides simultaneously. They are using Section 408(m) to move a portion of their retirement savings into physical gold — outside the stock market, outside the forced index rebalancing, outside the inflation spiral. And they are using 0% intro APR cards to eliminate the 22.76% interest that is draining their present-day cash flow. The combination creates a feedback loop: less money going to credit card interest means more money available for gold IRA contributions, which means more of your wealth is protected from the exact forces that are pressuring traditional portfolios right now.

Some of the best 0% intro APR cards (hands down)

The average American carries $6,700 in credit card debt at 22.76% APR — that’s $1,524/year in interest alone. Switch to a 0% intro APR card and pay no interest until 2027. Every payment goes toward your balance, not the bank.

Bottom Line

IRS Section 408(m) defines a legal framework that may allow certain retirement savers to move part of a 401(k), IRA, TSP, or 403(b) into physical gold and silver without triggering early-withdrawal penalties and while keeping retirement tax advantages intact. Most Americans have never even heard of it. Yet wealthy investors use strategies like this to protect gains, reduce exposure, and stay positioned when markets turn violent. With the Fed fractured 8-4, a new chair taking over in weeks, the SpaceX IPO triggering $33-52 billion in forced portfolio rebalancing, and inflation still above the 2% target, the pressures on traditional retirement portfolios are the most intense since 2008.

Gold has outperformed during every major crisis period in modern history: up 5% during the 2008 crash (while the S&P fell 38%), up 25% during the 2020 COVID year, and up 144% since the rate cut cycle began in 2024. Physical gold held inside a tax-advantaged retirement account provides genuine non-correlation to stocks, bonds, and the forced index rebalancing that the SpaceX IPO will impose on every passive investor. The 2026 contribution limit is $7,500, with a super catch-up of $8,600 for ages 60-63 — the highest in IRA history. It’s a legal, IRS-recognized framework — one that can help you protect retirement wealth without selling everything into cash.

Meanwhile, the average American carries over $6,700 in credit card debt at 22.76% APR — the highest rate in recorded history — costing $1,524 per year in interest alone. Total U.S. credit card debt crossed $1.2 trillion in 2026 with delinquencies rising for 11 consecutive quarters. But there’s a smarter move: Switch to a 0% intro APR card and pay no interest until 2027. That means your payment goes toward your balance—not high interest. Every dollar saved on credit card interest is a dollar that can be redirected toward building wealth.

The strongest financial position in 2026 addresses both the future and the present simultaneously: protecting retirement savings from inflation, forced rebalancing, and geopolitical risk through a 408(m) Gold IRA rollover, while eliminating the 22.76% credit card drain through 0% intro APR balance transfers. The two strategies create a feedback loop — less money to credit card interest means more available for gold contributions, more gold means more protection from the forces pressuring traditional portfolios. Both windows are open right now. Neither announces when it closes.