The IRS Loophole That Could Change Retirement Forever

In Partnership with

Hello and welcome to Deals Catchers - your briefing on the financial shifts shaping everyday life.

Today we’re breaking down a quietly powerful IRS rule that could dramatically change how Americans handle retirement income. It’s legal, it’s overlooked, and it’s already being used by those who understand how to navigate economic uncertainty.

A Retirement Strategy Hidden in the IRS Manual

Most Americans assume their retirement accounts - 401(k), IRA, TSP, 403(b) - are locked behind strict rules: early withdrawal penalties, tax burdens, and limited flexibility. But buried inside the tax code is IRS Section 408(m) - a provision allowing certain retirement assets to be reallocated into tangible stores of value, without triggering taxes or penalties.

What most people miss is the second part:

Once properly structured, this provision allows retirees to pull value from those assets as monthly or weekly income - completely tax-free.

It sounds like a myth, but it’s not.

It’s been available for years, just rarely discussed.

Why Ordinary Savers Never Hear About It

The financial industry has little incentive to promote strategies that reduce dependence on their products. 408(m) shifts power away from Wall Street by giving people the ability to generate income outside of stocks, bonds, or brokerage-controlled assets.

That means fewer fees, fewer middlemen, and more control.

For the industry, that’s a problem.

For regular Americans, it’s an opportunity.

The Real Appeal During Market Uncertainty

With market volatility returning and inflation eating into savings, traditional retirement accounts no longer feel as secure as they once did.

Section 408(m) offers something rare today:

income stability that isn't tied to market performance.

Most people won’t learn about this until it's too late.

But those who learn now can position themselves before the next downturn hits.

|

How Section 408(m) Actually Works

While the tax code is often confusing, 408(m) is surprisingly straightforward. It allows specific retirement assets to be redirected into tangible holdings recognized by the IRS. Once positioned correctly, those assets can be drawn against for tax-free income, unlike traditional withdrawals which can trigger taxes or compulsory minimum distributions.

In practical terms, this means retirees can establish a predictable second income stream without depending on stock performance, bond yields, or government policy shifts.

Why Wall Street Avoids Talking About It

Banks and financial institutions make billions managing retirement accounts. Mutual funds, brokerage fees, advisory fees, transaction costs - all of these depend on keeping people inside paper-based systems.

408(m) disrupts that.

It reduces Wall Street’s direct involvement.

It lowers reliance on market-based returns.

And it gives Americans the ability to protect wealth without paying layers of recurring fees.

For that reason, it’s rarely included in financial education, retirement training, or workplace seminars.

The Timing Couldn’t Be More Critical

Right now, several concerning trends are converging:

- Rising interest rates burden debt-heavy families

- Inflation erodes purchasing power

- Equities remain vulnerable to shocks

- Federal deficits pressure future tax policy

- Retirement accounts fluctuate with every market swing

When these forces combine, retirees face more exposure than they realize.

The ability to access income without taxes or penalties becomes a powerful safeguard.

Using 408(m) as a Protective Tool

This strategy is not about speculation.

It’s about:

- Stabilizing income

- Reducing tax liability

- Diversifying away from traditional market risk

- Preserving long-term purchasing power

For those nearing retirement - or already retired - the value of adding a tax-free income stream cannot be overstated.

Not a Loophole Forever

Tax strategies often disappear once they enter the public spotlight. As federal pressure for revenue grows, lesser-known provisions tend to be the first targets for revision.

That means the window to use 408(m) may not stay open indefinitely.

Those who move early lock in benefits that later retirees may lose.

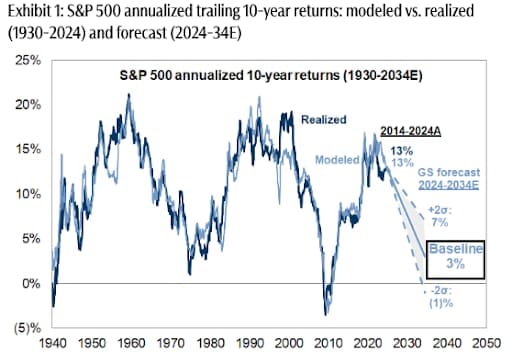

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

👉 My subscribers skip the waitlist

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

*AD

CLOSING THOUGHTS

As financial pressure builds across the country, Americans need tools that enhance stability, reduce exposure, and protect what they’ve earned. Section 408(m) offers an option that has been overlooked for too long - and those who act now gain an advantage that others may miss.

Thank you for reading today’s Deals Catchers briefing.

Stay informed, stay protected - and take control of your financial future.