The Digital Dollar Is Coming: What the Government’s CBDC Plan Means for Your Bank Account, Your Privacy, and Your Freedom

U.S. Government Digital Dollar Plan

We have urgent news… The U.S. government is moving forward with the Central Bank Digital Currency (CBDC) — and this may be your final opportunity to protect your cash and privacy.

Once this system is in place, the government will have full control over your money. They’ll decide what you can buy… how much you can spend… and they’ll be able to track every transaction you make.

But here’s the good news — there’s still time to legally “opt out” before the Digital Dollar becomes mandatory. Everything you need to know is explained step-by-step in this new, confidential guide.

Click here now to get your FREE copy before it’s taken down.

This may be your only chance to learn how to protect your savings, your privacy, and your family’s financial freedom before the switch is flipped. Don’t wait — every day you delay gives the government more power over your money.

| CLICK HERE TO CLAIM YOUR GUIDE NOW → |

Somewhere in Washington right now, a system is being built that will give the federal government the ability to see every dollar you spend, in real time, from the moment you spend it. It will know what you bought, where you bought it, and how much you paid. And if the government decides it does not approve of a transaction, it will have the technical capability to block it before it clears.

This is not a dystopian novel. It is a Central Bank Digital Currency — a CBDC — and the U.S. government is actively moving forward with the infrastructure to make it operational.

The implications for your financial privacy, your autonomy, and your ability to access your own money are enormous. And most Americans have no idea it is happening.

The window to understand what is being built — and to take steps to protect yourself before it becomes mandatory — is narrowing fast. Click here to claim your guide now (AD).

What a Digital Dollar Actually Means for You

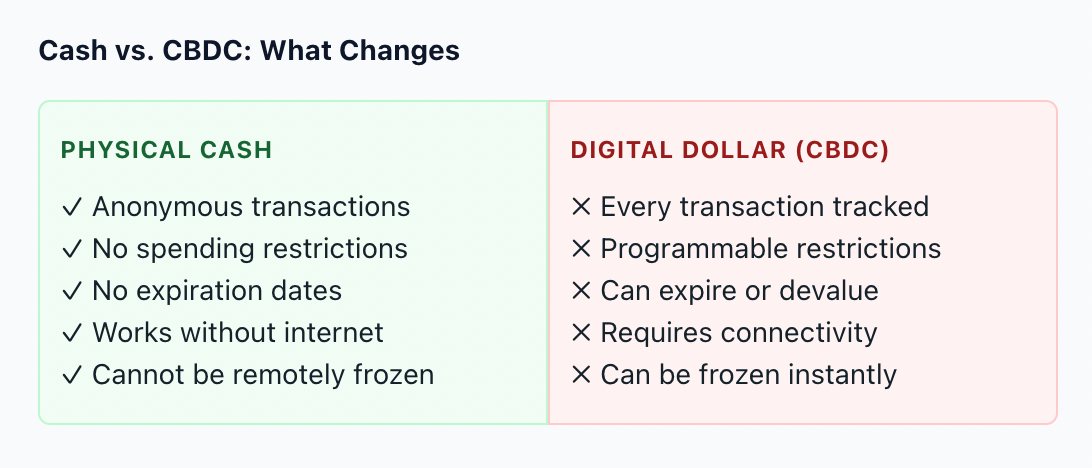

A Central Bank Digital Currency is not Bitcoin. It is not a cryptocurrency. It is the opposite. Bitcoin was designed to operate outside government control. A CBDC is designed to give the government maximum control over every unit of currency in circulation.

With a CBDC, the Federal Reserve would issue digital dollars directly. Every unit would be programmable — meaning the government could attach conditions to how it is spent. Expiration dates on stimulus payments. Restrictions on certain categories of purchases. Geographic limits on where your money can be used. All of this becomes technically possible when currency is digital and centrally controlled.

The shift from physical cash to a CBDC is not an upgrade. It is a fundamental transfer of control from the individual to the state. Cash gives you sovereignty over your money. A CBDC gives sovereignty to the issuer. The convenience of digital payments is being used as cover for what is, at its core, a surveillance and control mechanism.

Is Your Bank Safe?

Your bank doesn’t own the money in your account... YOU do. ...Right?

Well, that’s what most people think... But here’s the harsh truth: When you deposit money into a bank, you’re technically loaning it to them... And if that bank gets into financial trouble, they can use YOUR deposits to save their own skin.

It’s called a “bail-in” and it’s been 100% legal in America since 2010.

Find out more on the next page 👉 Is Your Bank Safe?

This isn’t conspiracy theory stuff... During financial crises, this exact thing happened in Cyprus in 2013 and in Lebanon in 2019. In Lebanon:

• There were more than $72 BILLION in losses...

• Depositors faced ~$400 monthly withdrawal restrictions on their accounts...

• And some even turned to armed robbery of their own banks in a desperate attempt to access their life savings.

Now, if you’re thinking this can happen in America because we’re “covered by FDIC insurance”... That’s true... But it’s only up to $250,000 per account... And here’s what they don’t advertise much: The FDIC’s “emergency” reserve fund holds just 1.28% of total insured deposits.

So, if multiple major banks failed simultaneously, that fund would likely be exhausted almost immediately. And during a true banking crisis, you could be standing in line with millions of other depositors waiting for a check that might take months (or years) to arrive...

That’s why you need to: Discover How Americans Are Protecting Their Savings in 2026 (Tap HERE to Request Your Free Wealth Protection Kit Now)

It’s time to find out how thousands are using gold & silver to help shield what they’ve spent decades building through hard work. Precious metals’ record-breaking run has spilled into 2026 as gold recently eclipsed $5,100 and silver hit $117... And just as they have for thousands of years, they could be well-positioned to continue helping protect accounts. Now is the time to prepare for the unexpected.

In this kit, you’ll find out:

• How to secure your assets from banks and institutions

• How to protect your buying power from the weakening dollar

• How to hedge against inflation and market volatility

• Why precious metals could be the ultimate form of insurance

You’ll also discover tips for whether this plan makes sense for your personal situation. No fees... no obligation... no pressure... Just good, clean information to help you and your family make informed decisions:

| Visit the next page HERE to request your complimentary kit → |

Your Bank Is Not as Safe as You Think

The CBDC conversation is happening against a backdrop that makes it even more alarming: the traditional banking system is more fragile than most people realize.

When you deposit money into a bank, you are technically lending it to them. If the bank gets into financial trouble, it can use your deposits to stabilize its own balance sheet. This is called a bail-in, and it has been legal in the United States since 2010. Most depositors have no idea this mechanism exists.

FDIC insurance covers up to $250,000 per account — but the FDIC’s emergency reserve fund holds just 1.28% of total insured deposits. If multiple major banks failed simultaneously, that fund would be exhausted almost immediately. During a true banking crisis, depositors could wait months or years to receive their insured funds.

This is not theoretical. In Cyprus in 2013, depositors lost up to 47.5% of uninsured balances overnight. In Lebanon in 2019, there were more than $72 billion in losses, depositors faced strict withdrawal limits, and some resorted to desperate measures to access their own savings.

A CBDC layered on top of an already fragile banking system does not make things safer. It makes the government’s ability to freeze, restrict, or redirect your money faster and more seamless than ever before. Click here to claim your guide now (AD).