The Digital Dollar Countdown: What Washington Just Confirmed, What They’re Not Telling You, and the Gold Loophole That Closes When the Switch Flips

Trump’s Dirty Secret

Trump messed up on stage once again.

His staff was embarrassed and covered their faces… This time his mental faculties failed him again.

What did he do exactly?

Trump slipped up and named the day the government will dump the US dollar And bring in the new digital dollar system That gives them full control over YOUR money.

| Get All The Details HERE>>> |

This is an advertisement. If you no longer wish to receive promotional messages from this advertiser, please unsubscribe below. Or write to: 5005 Lyndon B. Johnson Fwy. Suite 350 Dallas, TX 75244

* Sponsored by Priority Gold

There are moments in politics where the mask slips. Not through a leaked document or a whistleblower — but through a simple, unguarded statement on a public stage. The kind of moment that gets scrubbed from the official transcript within hours but lives forever on the internet.

Washington just had one of those moments. And what was revealed — however briefly — confirmed what financial insiders have been warning about for years: the U.S. government is actively moving toward replacing the dollar as you know it with a fully digital system that gives them unprecedented control over every transaction in the economy.

The infrastructure is not theoretical. FedNow is already live, processing transactions in real time 24/7. The CBDC framework is being built on top of it. And the legal authority to execute the transition exists right now — it does not require an act of Congress.

Most Americans have no idea how far along this process is, or what it means for their ability to access and control their own money.

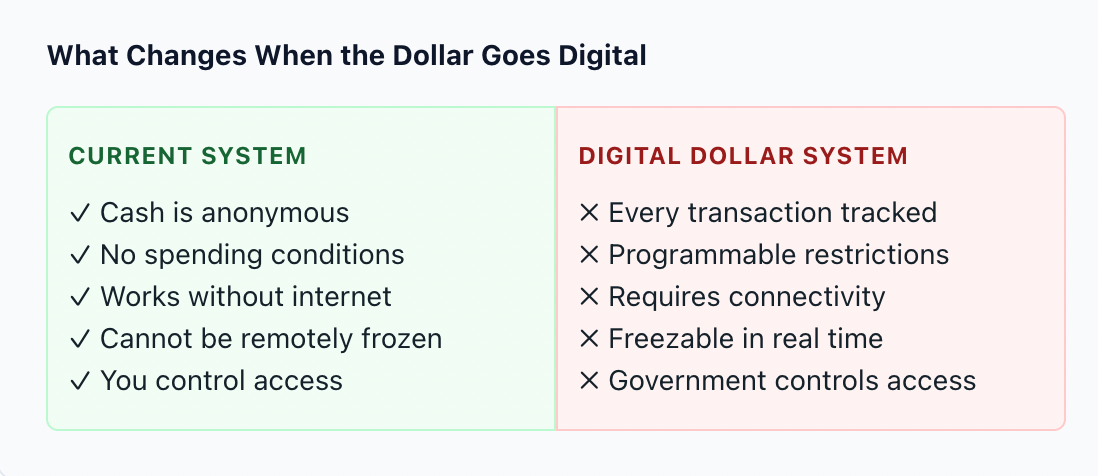

What a Digital Dollar System Actually Gives Them

The shift from physical cash and traditional banking to a Central Bank Digital Currency is not a technological upgrade. It is a fundamental transfer of power from the individual to the state.

With a CBDC, the government gains the ability to track every transaction you make in real time. Not through a warrant or a court order. By default. The system is designed so that every unit of currency carries a complete record of where it has been, who held it, and what it was spent on.

But surveillance is only the beginning. A digital dollar is programmable. That means the issuer — the Federal Reserve — can attach conditions to the currency itself. Expiration dates on stimulus payments so you must spend them within a window. Category restrictions that prevent purchases the government deems undesirable. Geographic limits that confine your money to approved regions. Spending caps that limit how much you can transact in a given period.

None of this requires conspiracy theories. The capabilities are inherent in the technology. A digital currency issued and controlled by a central authority can be programmed — that is a feature, not a bug. The question is not whether the government could do these things. It is whether you trust every future administration to choose not to.

The Infrastructure Is Not Coming — It Is Already Here

The Federal Reserve’s FedNow system went live in 2023. It processes transactions instantly, 24 hours a day, 365 days a year. Unlike the legacy ACH system, which batched payments overnight and created a buffer between transaction and settlement, FedNow eliminates that buffer entirely.

This is not coincidental timing. FedNow is the settlement layer that a CBDC requires to function. You cannot have programmable, real-time digital currency without a real-time settlement system to process it. The infrastructure was built first — deliberately, quietly, and without public debate — so that when the digital dollar is deployed, the pipes are already in place.

The 93-page regulatory docket (OP-1670) that authorized FedNow established the Federal Reserve’s most granular interaction with the national payment grid in the institution’s history. Financial analysts who have reviewed it describe capabilities that go beyond mere payment speed: transaction-level monitoring, centralized processing, and the architectural foundation for instant intervention.

The system is live. The CBDC layer is being built on top of it. And the timeline for full deployment may be shorter than most people assume.

The gold accounting trick Washington hoped you’d never notice.

We printed 1,000 copies of this report. 688 are gone. When the last one goes out, we’re pulling it offline — the information inside is too sensitive to leave up indefinitely.

Here’s what’s inside the remaining copies: The executive order Trump can sign tomorrow — the same legal authority FDR used in 1934 to move billions in wealth overnight — and exactly how to position before it happens.

This isn’t a newsletter. It’s not evergreen content. It’s a window. And 688 people already jumped through it.

Claim one of the 312 remaining copies →

We won’t reopen this once it’s closed.

| Get my copy now → |

* Sponsored by Allegiance Gold

This Has Happened Before — In 1934

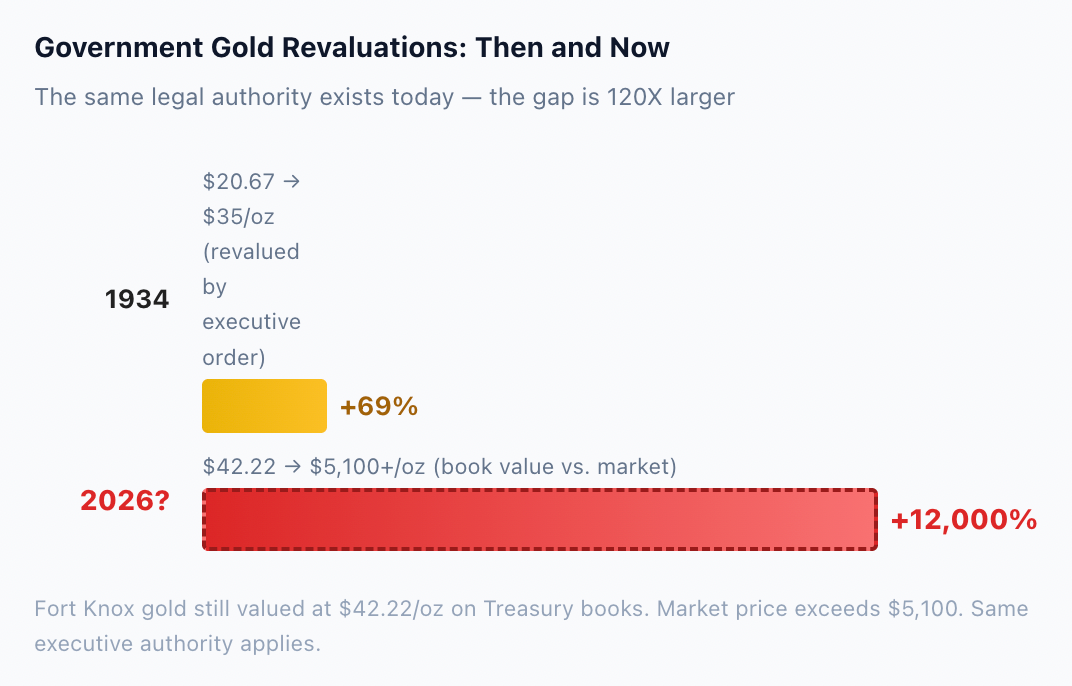

Most Americans do not know that the U.S. government has already executed a sweeping seizure of private wealth tied to currency reform. In 1933, Franklin Roosevelt signed Executive Order 6102, making it illegal for American citizens to own gold. Violators faced up to 10 years in prison and $10,000 in fines — the equivalent of roughly $230,000 today.

Citizens were required to surrender their gold to the Federal Reserve at a fixed price of $20.67 per ounce. Then, in 1934, Roosevelt signed the Gold Reserve Act, which revalued gold to $35 per ounce — an instant 69% devaluation of every dollar in circulation. The government gained billions in value overnight. The citizens who surrendered their gold lost purchasing power they would never recover.

The legal authority Roosevelt used in 1934 still exists. It has never been repealed. The President can revalue the gold on the Treasury’s balance sheet with a single executive action — no Congressional approval required. The only difference is scale: in 1934, the gap was 69%. In 2026, the gap between the book value ($42.22/oz) and the market value ($5,100+/oz) is over 12,000%.

Why a Revaluation May Be Inevitable

The U.S. national debt now exceeds $36 trillion. Interest payments alone consume a growing share of the federal budget. And the government is running out of conventional tools to manage the fiscal crisis without triggering inflation, raising taxes to politically unacceptable levels, or defaulting on obligations.

A gold revaluation solves multiple problems simultaneously. By marking the 8,133 tonnes of gold in Fort Knox to market — from $42.22 to $5,100+ per ounce — the Treasury would instantly add approximately $750 billion to its balance sheet without printing a single dollar, raising a single tax, or borrowing from a single creditor.

It would also serve as the monetary reset that a CBDC transition requires. When you are replacing the existing dollar with a digital version, establishing a hard asset anchor for the new currency gives it credibility that pure fiat cannot achieve. This is why central banks around the world have been buying gold at record levels — they are preparing for exactly this kind of reset.

The executive order that enables this revaluation uses the same legal authority FDR invoked in 1934. The mechanism is well understood. The only question is timing.

What Happens to Gold When the Reset Arrives

If the government revalues its gold holdings to market, it does more than fix a balance sheet. It sends an unmistakable signal to every institutional investor, central bank, and sovereign wealth fund on the planet: the United States officially recognizes gold as a monetary asset at its true market value.

That signal would trigger a repricing event across the entire precious metals market. Institutional capital that has been sitting on the sidelines — pension funds, insurance companies, endowments that are restricted from holding gold until it is formally acknowledged as a reserve asset — would flood in. The supply of physical gold is finite and cannot be expanded. The demand shock would be unlike anything the metals market has experienced since the 1970s.

Gold is already at $5,100. The question is not whether it goes higher. The question is whether the move to $7,000, $10,000, or even $15,000 happens gradually over years — or violently over weeks when the revaluation announcement hits. History suggests the latter.

The Convergence: Digital Dollar + Gold Reset + Your Bank Account

These three events — the digital dollar deployment, the gold revaluation, and the real-time surveillance infrastructure — are not separate stories. They are one story playing out across multiple timelines, all converging on the same conclusion: the financial system you grew up with is being replaced.

The old system gave you privacy. The new system gives the government visibility. The old system let you hold cash outside the banking grid. The new system is designed to bring every dollar inside a centralized, trackable, programmable network. The old system valued gold at a number set in 1973. The new system will have to acknowledge what the market already knows.

The Americans who navigate this transition successfully will be the ones who understood what was coming and positioned themselves before the switch was flipped. The ones who assumed the current system would last forever will discover that the rules changed while they were not paying attention.