The 2033 Retirement Cliff: What Washington Just Confirmed and What You Can Still Do About It

Trump’s Retirement Revolution: Secure Your Future Now

Retirees, listen up: President Trump’s back, and your golden years just got a major upgrade. His bold economic moves—extending the 2017 tax cuts and unleashing deeper reforms—could flood your pockets with cash and unlock insane wealth-building potential.

But here’s the catch: traditional 401(k)s, IRAs, and TSPs? They’re ticking time bombs. One market crash, one shady manipulation, and poof—decades of savings, gone.

Trump left you a lifeline—a wealth-protection secret the IRS doesn’t want you to know. It’s your chance to shield your retirement from chaos, tax-free and penalty-free, with a rock-solid strategy.

| Grab our 2026 Wealth Protection Guide—FREE today → |

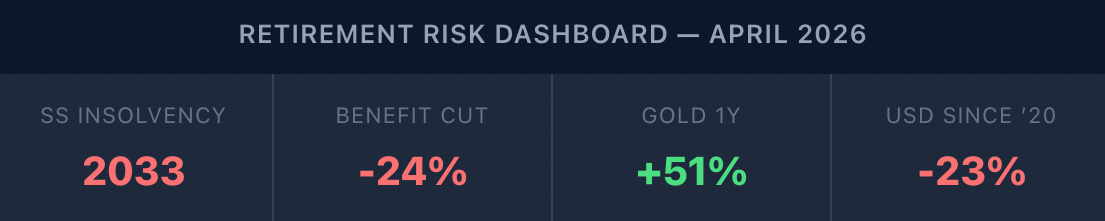

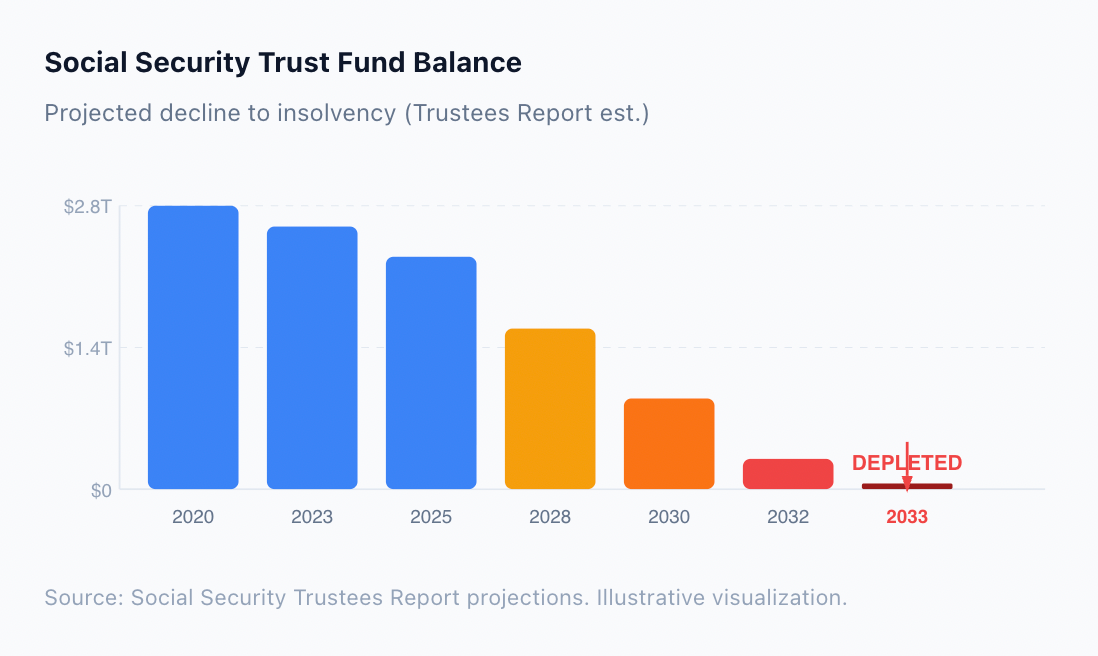

There is a number that should be keeping every American over 50 awake at night: 2033.

That is the year the Social Security trust fund is projected to run dry. Not according to bloggers or conspiracy theorists — according to Washington itself. The trustees’ own report lays it out in black and white, and the math has not improved.

Seven years. That is all the runway that is left before the system that 67 million Americans depend on hits a wall. And when it does, the consequences are not abstract — they are automatic, immediate, and devastating.

For most retirees, the plan was simple: work for decades, save what you can, count on Social Security to fill the gap. That plan is now on a collision course with arithmetic that does not care about promises.

What “Insolvency” Actually Means for Your Check

Insolvency does not mean Social Security disappears overnight. It means the trust fund can no longer cover the gap between what comes in through payroll taxes and what goes out in benefits. When that happens, the law requires benefits to be cut to match incoming revenue.

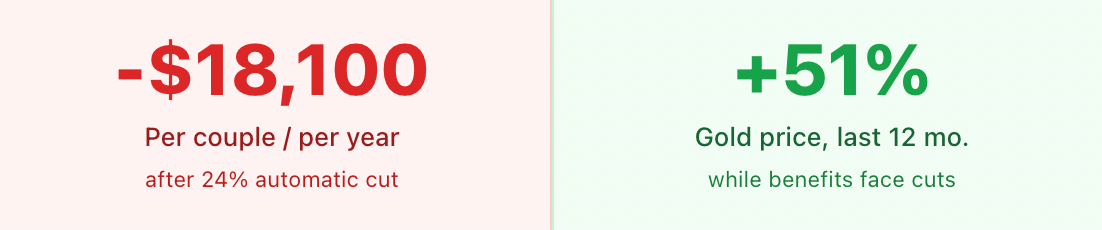

The projected cut? Roughly 24 percent — across the board, for every recipient. For a typical retired couple, that translates to approximately $18,100 less per year. Not phased in over a decade. Not means-tested. Just gone.

Congress could act to prevent this, of course. But Congress has known about this timeline for over twenty years and has done nothing. The political incentive is to push the problem past the next election cycle, and the next one, and the next one — until the math forces the issue.

Meanwhile, the retirees who built their entire financial plan around that check are left to wonder whether the promise will be kept.

The Problem Is Bigger Than One Program

Social Security is not the only pillar under stress. Traditional retirement accounts — 401(k)s, IRAs, TSPs — are tied directly to markets that have grown increasingly volatile and unpredictable. One bad year at the wrong time can erase a decade of compounding.

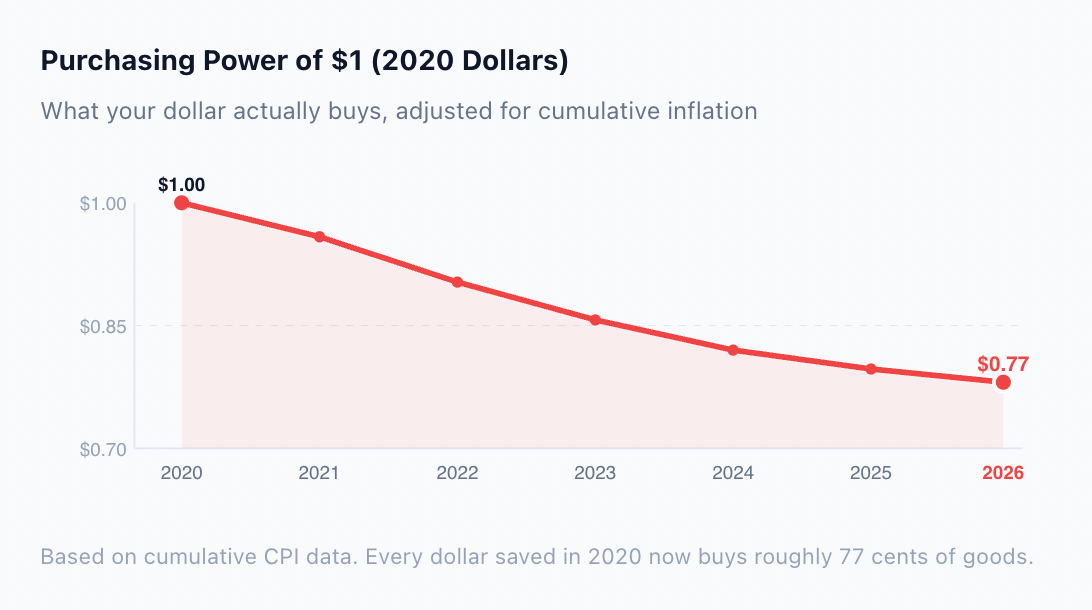

The 2020s have already delivered a masterclass in how quickly things can go sideways. Pandemic shutdowns. Banking failures. Inflation that eroded purchasing power faster than interest could replace it. Supply chain disruptions that drove the cost of essentials — food, insurance, housing — to levels that retirement planning models never anticipated.

For retirees, this creates a two-front problem: the income you were promised may shrink, and the savings you have may not stretch as far as you thought. Both at the same time.

What Is Changing — and What Is Not

On the policy front, there are moves underway that could reshape the retirement landscape. The push to extend the 2017 tax cuts and introduce deeper economic reforms has real implications for how retirees can structure their wealth. If enacted, these changes could create windows of opportunity for tax-advantaged moves that were not available before.

But policy windows close. They always do. The retirees who benefit are the ones who position themselves before the rules change — not after.

What is not changing is the fundamental vulnerability: if your entire retirement is held in accounts that depend on market performance and government solvency, you are exposed to risks that no amount of diversification within those systems can eliminate.

Social Security robbed and you’re paying the price

Washington just confirmed what nobody wanted to say out loud: Social Security is going broke. It will hit insolvency by 2033 — triggering an automatic 24% cut to EVERY retiree’s check in seven years. For a typical couple, that’s $18,100 LESS per year. Gone. Overnight.

And that’s before further gutting of this agency. Before impeachment chaos freezes Washington solid. Your check was never guaranteed. Now it seems to be on shakier grounds than ever.

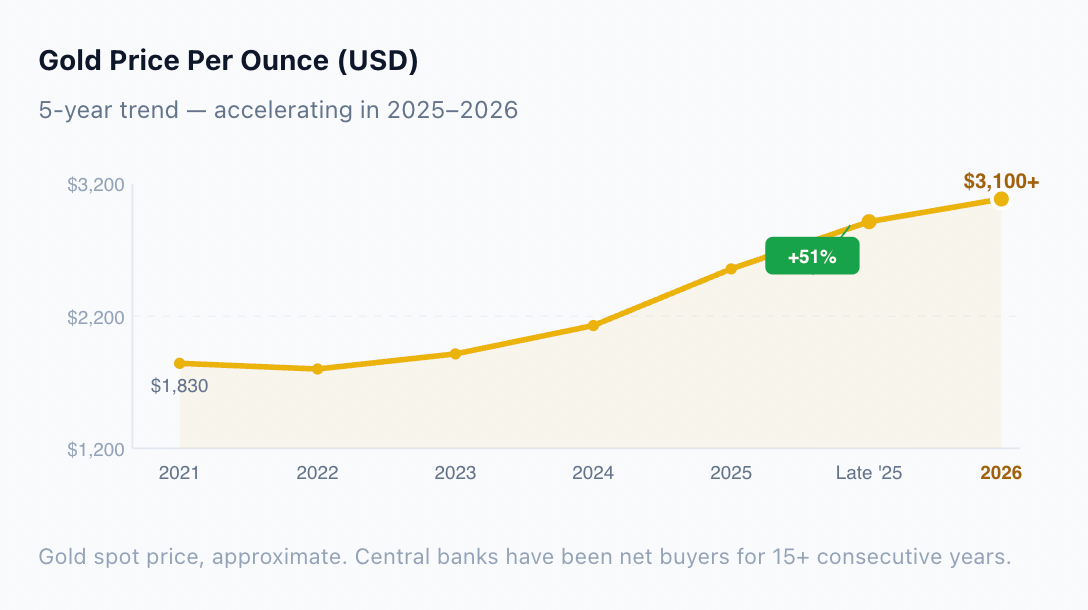

Gold doesn’t get cancelled. Last year it surged 51%. Central banks are loading up. Billionaires are loading up.

We spent months compiling everything into one FREE Gold Guide — tax-free IRA rollover steps, a loophole Washington doesn’t advertise, and exactly what smart retirees are doing right now.

| Claim My Free Gold Guide » |

Why Retirees Are Quietly Moving to Hard Assets

There is a reason gold keeps coming up in conversations about retirement protection, and it is not nostalgia. It is math.

Gold surged over 50 percent last year alone. Central banks around the world have been accumulating it at a pace not seen in decades. Billionaire investors who built their fortunes in equities are rotating a portion into physical metal. These are not emotional decisions — they are calculated hedges against a system that is showing cracks at every level.

The logic is straightforward: when the institutions that print money are stockpiling the one asset that cannot be printed, that tells you something about where the smart money sees risk.

For individual retirees, the appeal goes beyond price appreciation. Physical gold is not a login. It is not a balance on a screen that depends on a server staying online. It is not subject to the processing delays, policy freezes, or systemic failures that have rattled the banking sector in recent years. It is a hard asset you own outright — one that has preserved purchasing power through every crisis on record.

Seven Years Is Not as Long as It Sounds

The 2033 insolvency date is not a prediction that might be revised away. It is the baseline scenario in the trustees’ own modeling — and many independent analysts believe the actual timeline could be shorter if economic growth slows or unemployment rises.

Seven years sounds like plenty of time, until you consider that meaningful financial restructuring — rollovers, reallocations, tax planning — takes months to execute properly. The window for calm, strategic action is now. Not when the headlines turn panicked and everyone is scrambling for the exits at the same time.

The retirees who will weather what is coming are the ones who took the time to understand their exposure and made deliberate moves to reduce it — not out of fear, but out of the same clear-eyed pragmatism that has always separated those who preserve wealth from those who lose it.

If your retirement plan depends entirely on promises from Washington and balances held inside a system you do not control, this is the moment to ask whether that plan still makes sense.

Share this with someone who still believes their check is guaranteed. The trustees’ own report says otherwise.