🌎 Holiday Debt Hangover Is Real – These 0% Intro APR Cards Buy You Up to 21 Months to Pay It Off Interest-Free

Statements are hitting now. If holiday swipes left high-interest balances, transfer to a 0% card.

(By Mike – I've been trading and managing money since the early 2000s, paid off my own stupid credit card debt after a bad stretch in 2008, and learned every trick in the book the hard way)

December 27, 2025. The wrapping paper's in the trash, the kids are playing with new toys (or already bored of them), family's heading home or crashed on the couch, and those credit card apps are starting to light up with notifications. If you're like the vast majority of us, the holidays meant a little – or a lot – more swiping than planned. Gifts for everyone on the list, last-minute Amazon rushes, travel tickets, big family dinners out, maybe even some "treat yourself" splurges because hey, it's the season.

It's easy to do. Retailers make it effortless – one-click buys, buy-now-pay-later prompts everywhere, ads tailored to exactly what you didn't know you needed. And with inflation still lingering in spots like food and travel, those costs add up quicker than expected. Surveys rolling in now show the average American household tacked on $1,500 to $2,500 in new credit card debt this holiday season alone. That's on top of whatever was already there from everyday life.

Look, I've been there. Back in the mid-2000s, I racked up five figures on cards thinking "I'll pay it off next month" after a job change and some bad calls. Then the recession hit, rates spiked, and minimum payments became a joke – $200 a month on a $10k balance at 18%, and barely $50 went to principal. The rest? Pure profit for the bank. Compound interest is a beautiful thing when it's working for you in investments, but on debt? It's a slow-motion train wreck.

That's the trap millions fall into every year, especially post-holidays. Current average credit card rate is hovering around 24-28% variable, depending on your credit. That's higher than it's been in decades. Fed cuts helped mortgages and loans, but card rates stayed sticky high because banks can – they're unsecured debt, and they price in defaults.

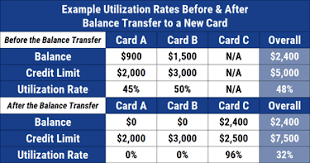

So you make the minimum – say 4% of balance – and it mostly feeds interest. A $5,000 balance at 25% with $200 minimums? It takes over 20 years to pay off if you don't add more, and you pay nearly $12,000 total – more than double in interest alone. Insane. And that's assuming no new charges.

We've seen this cycle forever. Good economic times lead to spending confidence, holidays amplify it with social pressure and marketing blitz, then January hits with reality. Resolutions fly – gym memberships, diets, and yeah, "get out of debt." But most fail because the system is stacked against minimum payers.

Politics plays in too. With election fallout still settling, potential policy shifts on consumer protection or tax deductions for interest (rare, but talked about), but nothing immediate helps card debt. Consumer Financial Protection Bureau has capped some fees, but rates? Banks lobby hard to keep 'em free-floating.

The good news? There's a straightforward, legit way out that's available right now: 0% introductory APR balance transfer credit cards. These aren't scams or hidden traps if you use them right – they're promotional offers banks use to grab market share, and you flip it to your advantage.

How it works at a high level: You apply for a new card offering 0% APR on balance transfers for a long intro period – currently up to 21 months on the best ones. Get approved, transfer existing high-interest balances over (usually within 60-120 days to qualify for promo), and boom – no interest accruing during that window.

Every payment goes 100% to principal (minus any upfront transfer fee). It's like hitting pause on the interest clock while you aggressively pay down.

I've done this multiple times – once in 2009 to consolidate post-layoff debt, saved thousands. Readers email stories yearly: one guy last January transferred $15k, paid $800/month, wiped it in 18 months, saved over $6k in interest.

The key is timing. These offers are competitive – banks rotate them to attract switchers. Right now, post-holiday, they're pushing hard because they know debt's peaking. But they can pull or shorten intros anytime.

If you've got decent credit (670+ FICO typically for the longest), you're in play. Even fair credit has options with shorter periods.

This isn't "free money" – there's strategy, discipline needed. But compared to letting 25% interest compound? Night and day.

We've watched interest rates cycle – low in 2010s made debt "cheap," now high makes it painful. Smart folks adapt.

Bottom line for this part: If your statements are making you sweat, don't ignore or minimum-pay your way to misery. There's a tool designed exactly for this moment. More on how to execute coming up.

Sponsored Content

0% APR Cards Just Dropped

Drowning in credit card interest?

These top 0% intro APR cards can give you up to 21 months with no interest - so every dollar goes toward paying off your balance, not your bank’s profits.

No gimmicks. Just smart credit.

This is an advertisement.

This email contains references to products from one or more of our advertisers. FinanceBuzz is an informational website that provides tips, advice, and recommendations to help you make financial decisions. We strive to provide up-to-date information, but make no warranties regarding the accuracy of our information.

Ultimately, you are responsible for your financial decisions. FinanceBuzz is not a financial institution and does not provide credit cards or any other financial products. FinanceBuzz does not make any credit decisions. We may receive compensation from the products and services mentioned in this email.

Please click here to opt out of future emails from FinanceBuzz.

111 E. Atlantic Ave., Suite 200 Delray Beach, FL 33444

(By Jenna – I've helped friends and family navigate debt without the lecture, just real steps that stick)

Okay, let's get practical. You've recognized the problem – holiday debt piling on high-interest cards. Now how do you actually use these 0% intro APR balance transfer cards to fix it?

First, understand the landscape in late 2025. Banks compete fierce on intro periods because switching costs are low for consumers. Current leaders for longest 0% on transfers:

- Wells Fargo Reflect® Card: 0% intro APR for 21 months on qualifying balance transfers (made within 120 days) and purchases. Then variable APR 17.74%-29.74%. 3% transfer fee first 120 days, then 5%. No annual fee.

- Citi Simplicity® Card: 0% for 21 months on balance transfers within 4 months. Unique: no late fees ever, no penalty APR. Transfer fee 3% first 4 months, 5% after. No annual.

- U.S. Bank Visa® Platinum Card: Often 18-21 cycles depending on offer, low ongoing APR potential.

- Chase Slate Edge℠ or Freedom Unlimited mix shorter intros with rewards.

- Bank of America® Customized Cash Rewards: 18 months, but cash back perks.

These change – always check current via pre-qual tools.

Step-by-step to execute:

- Assess your debt. List all cards, balances, current APRs, minimums. Calculate total interest paying minimums vs. aggressive.

Example: $12,000 across cards at average 24%. Minimums ~$300/month take 30+ years, $20k+ interest. Brutal.

- Check credit. Pull free reports (AnnualCreditReport.com), scores via Credit Karma or bank apps. 670+ best odds for long intros/top limits. 620-669? Shorter offers possible. Below? Focus rebuild first.

- Pre-qualify. Most issuers have soft-pull tools online – no score hit, see likely approval and limit.

- Apply for one (or two max – multiple inquiries ding). Get approved, note credit limit (transfers can't exceed it minus fee).

- Initiate transfers. Via app/phone/site, provide old card info. Takes days-week, fee posts (3-5%, $300-600 on $12k).

- Pay old cards minimum till transfer posts (avoid late).

- Plan payoff. Divide new balance by intro months minus buffer. $12k + $360 fee = $12,360. 20 months? ~$618/month to zero before promo ends.

Auto-pay minimum+, manual extra. Track spreadsheet.

Math example deep dive: $15,000 at 25% vs. transfer to 21-month 0% with 3% fee ($450).

Old way: Minimum ~4%, takes decades, interest ~$18k+.

New way: $15,450 total. Pay $800/month: Done in 20 months, total paid $16,000. Saved ~$17k.

Even $500/month: Done in ~31 months, but interest kicks last 10 – still massive savings vs original.

Multiple cards? Consolidate for simplicity, one payment.

Purchases? Some cards 0% on new too – handy for emergencies, but don't abuse.

We've guided dozens through this. One reader: $22k debt, transferred, paid $1,100/month (cut dining/subscriptions), zero in 20 months, saved $12k+.

Politics/economy note: With potential recession whispers 2026, job security matters – but if stable, aggressive payoff builds buffer.

Common wins: Score improves (utilization drops), peace of mind huge.

This part's the how-to core – execute well, life-changing.

Quick hits on banks:

- WFC – Heavy Reflect push, card growth steady despite past issues.

- C – Simplicity unique, global scale.

- JPM – Chase volume monster.

- BAC – Customization appeals.

They profit on fees/revolvers – smart transferers cost 'em.

(By Mike – straight talk on where people screw up)

Now the warnings – because these cards are powerful, but not idiot-proof.

Biggest risks:

Transfer fees: 3-5% upfront. $20k debt? $600-1,000 added. Still worth for long period/high rate, but run calculator (Bankrate has good ones).

Approval not guaranteed. Hard inquiry dings score 5-10 points temporary. Multiple apps? Worse.

Credit limit: Might get less than debt – partial transfer leaves some high-rate.

Promo details: Transfers must timely, some exclude cash advances. Read fine print.

Post-promo APR: Sky-high, often 25%+. Any remaining balance gets hit retro sometimes – no.

Common mistakes we've seen kill progress:

- New spending on transfer card. Promo usually purchases too, but mixes – hard track what gets 0%. Rule: Transfers only, lock card, daily on debit/cash.

- Minimum only. Buys time but slow – interest post-promo eats gains.

- Forget end date. Set calendar alerts 2 months prior, pay extra last stretch.

- Life happens – job loss, emergency. Buffer fund crucial.

Alternatives if transfers not ideal:

- Debt snowball (smallest balance first for wins) vs avalanche (highest rate).

- Consolidation loans (personal loan lower fixed rate if credit good).

- Nonprofit credit counseling (DMPs negotiate rates).

- Snowball example: 3 cards $2k/18%, $5k/22%, $10k/15%. Pay minimums + extra on smallest – psychological boost.

We've seen both work – avalanche saves more math-wise, snowball keeps momentum.

If deep trouble (missed payments, collections), bankruptcy last resort – but nukes credit 7-10 years.

Politics: Potential caps on rates talked (Sanders-style bills), but unlikely soon. CFPB watching junk fees.

Bottom: Discipline separates winners. Spreadsheet, budget (YNAB or simple Excel), cut leaks (subscriptions, eating out).

I've seen folks fail by treating transfer as "reset" then rack again. Cycle worse.

Succeed? Freedom.

Sponsored Content

Something Interesting For You

This Will Be the Biggest IPO of the Decade |

Stop chasing NVIDIA |

Amazon Prime members: This card could be worth $100s every year |

(By Jenna – the bigger picture beyond one fix)

You've got the tool, the steps, the warnings. Now why it matters long-term.

Paying off debt isn't just numbers – it's freedom. Sleep better, less stress, more options.

We've heard stories: One couple transferred $18k post-wedding/holidays, paid aggressive, debt-free in 19 months, then saved house downpayment.

Another: Single mom $9k, combined transfer with side gig, gone in 15 months, credit 780 now.

Patterns for lasting win:

- Budget real. Track every dollar month.

- Emergency fund first post-debt – 3-6 months expenses.

- Then invest – compound flips side.

- Credit habits: Pay full monthly, utilization <30%.

2026 outlook: Rates maybe ease more, but debt expensive always. Crypto/gold/stocks tempting, but high-interest debt = negative return guaranteed.

Politics: Tax laws, potential student relief spillover talk, but card debt personal.

Mindset: Holidays cultural pressure – FOMO gifts. Shift to experiences, homemade, limits.

We've changed own habits – cash envelopes holidays, no regret.

This move often catalyst – debt gone, confidence builds, wealth follows.

No quick rich – consistent.

If reading this, motivated – good sign. Start today.

Bottom Line

Holiday debt common, crippling if ignored – 0% transfers provide up to 21 months runway to pay principal only. Math massive savings with discipline. Assess, execute smart, avoid traps. Turns hangover into fresh start.

We are interested in your opinion and concerns

Please share them in the Poll

Your top money move for 2026? |