Musk Just Fired 6,700 IRS Agents. Inflation Just Hit 0.6% in One Month. Your Retirement Is Caught in the Middle.

Trump’s IRS rule still shields retirement money — for now

Elon Musk Just Declared War on the IRS. Your 401(k) Is Caught in the Crossfire.

Elon Musk just did what no one else dared. He challenged the IRS head-on — and took out over 6,700 federal enforcers in one sweep.

This isn’t a publicity stunt. It’s the start of a financial shakeup that could unravel the retirement system millions rely on.

Why? Because the IRS is more than a tax collector — it’s the gatekeeper of your money. And now that gate is cracked wide open.

But here’s what they’re not telling you on CNBC… Before Musk disrupted the system, Trump quietly left behind a legal IRS backdoor. A loophole designed to help Americans move their retirement savings out of government-controlled accounts — before things implode.

It’s real. It’s legal. And it’s still active.

Here’s what you need to know: Here’s a way to shift your IRA or 401(k) into a tax-advantaged, penalty-free vehicle that isn’t tied to Wall Street or federal policy changes. It’s outlined in the 2026 Wealth Preservation Guide — now available for free.

• No taxes

• No penalties

• No IRS strings

Just a smarter move while the window is still open.

Click here to claim your free guide now.

Because Elon’s not waiting. Neither should you.

P.S. If Musk just fired the agents… who’s guarding your money?

| Get the guide → |

If you no longer wish to receive promotional messages from this advertiser, please unsubscribe below. Or write to: 5005 Lyndon B. Johnson Fwy. Suite 350 Dallas, TX 75244

Two events happened within days of each other that, taken together, paint a picture most Americans are not seeing. First, Elon Musk — through his role in restructuring federal agencies — removed over 6,700 IRS enforcement agents from their positions. Second, the March 2026 inflation report came in at +0.6% in a single month — a pace that annualizes to 7.2%.

On the surface, these look like unrelated stories. One is about government downsizing. The other is about consumer prices. But for anyone with a 401(k), an IRA, or a TSP, these two events are converging on the same conclusion: the retirement system you rely on is being reshaped from the inside out, and the protection mechanisms you assume are in place may not be there much longer.

The window to act while the existing rules still apply is narrowing by the day.

Elon Musk just did what no one else dared. He challenged the IRS head-on — and took out over 6,700 federal enforcers in one sweep. This isn’t a publicity stunt. It’s the start of a financial shakeup that could unravel the retirement system millions rely on. But here’s what they’re not telling you on CNBC… Before Musk disrupted the system, Trump quietly left behind a legal IRS backdoor. A loophole designed to help Americans move their retirement savings out of government-controlled accounts — before things implode. It’s real. It’s legal. And it’s still active. Get the guide. Shield your future. While it’s still legal (AD).

What 6,700 Missing IRS Agents Actually Means for Your Money

The IRS is not just a tax collection agency. It is the enforcement arm of the entire retirement account system. It polices contribution limits. It enforces withdrawal rules. It audits rollovers. It monitors required minimum distributions. Every rule that governs how your 401(k) or IRA operates is ultimately enforced by the IRS.

When you remove 6,700 enforcement agents in one sweep, you create a gap — not in tax collection, but in the system’s ability to monitor and enforce the rules that govern retirement accounts. For most Americans, this creates uncertainty. The rules on paper remain the same. But the agency that enforces them has been significantly weakened.

This creates a paradox. The weakened enforcement environment actually makes certain legal loopholes more valuable — because the window to use them is wider while the agency that normally scrutinizes them is operating at reduced capacity. The Americans who understand this dynamic are repositioning right now, while the rules still favor them.

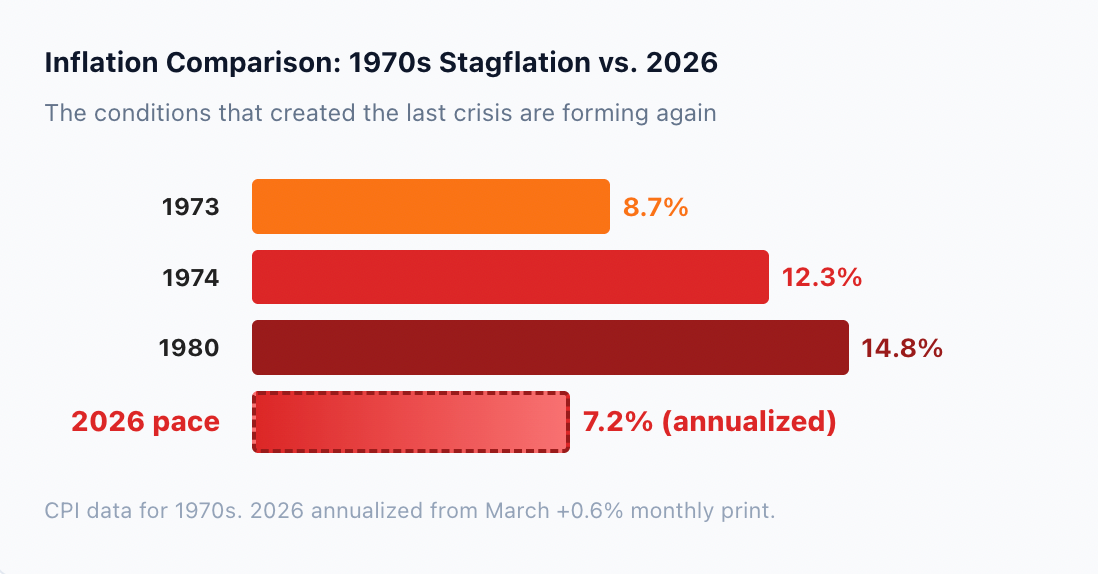

0.6% in One Month. The 1970s Playbook Is Repeating.

Most Americans glanced at the March inflation number and moved on. They should not have. A 0.6% monthly print is not business as usual. If inflation continues at this pace, the annualized rate hits 7.2% — a level the country has not sustained since the stagflation crisis of the 1970s.

The parallels to the 1970s are uncomfortable. Two simultaneous wars are straining the global supply chain. Energy prices are spiking. The national debt has passed $38 trillion. And the Federal Reserve is trapped between cutting rates (which fuels inflation) and maintaining rates (which crushes the economy). The same impossible position Arthur Burns faced in 1974.

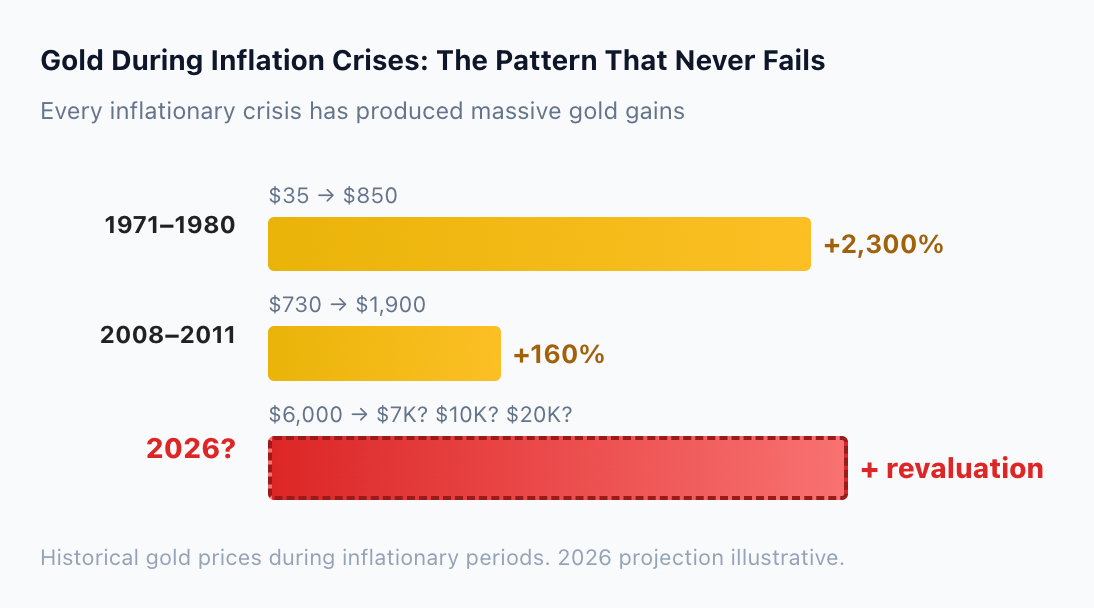

Here is what happened during the last stagflation crisis that most people have forgotten: the stock market lost 92% of its real (inflation-adjusted) value. Savings accounts were destroyed. The purchasing power of every dollar in a retirement account was crushed. But gold — gold went from $35 in 1971 to $850 in 1980. A 2,300% gain while everything else collapsed.

The $42 Accounting Fiction and the Coming Gold Reset

The 1970s parallel gets even more uncomfortable when you add the gold revaluation angle. The U.S. government holds 8,133 tonnes of gold in Fort Knox, valued on the Treasury’s books at $42.22 per ounce — a price set in 1973. At today’s market price above $6,000, the accounting gap is massive. And the President has the legal authority to close it with a single executive order.

Trump has publicly questioned why America doesn’t “use” its gold. The conditions that would justify invoking the revaluation authority are mounting: inflation at 7.2% annualized pace, a $38 trillion national debt, two active wars, and a weakening dollar. When the revaluation happens, it will not be gradual. It will be the largest wealth transfer in modern history. The investors already positioned in gold will be on the right side. Everyone else will watch.

Inflation Just Exploded 0.6% in ONE MONTH. The 1970s Playbook is Repeating

March 2026: +0.6% inflation in a single month. Most people don’t realize they just witnessed the opening shot of the next great monetary crisis.

If inflation continues at this pace, we’re looking at 7.2% annual inflation.

Here’s what happened the last time America faced this scenario: The 1970s Stagflation Crisis. Inflation hit 14%. The stock market lost 92% of its real value. Savings accounts were destroyed. But one asset gained 2,300%. Gold. From $35 in 1971 to $850 in 1980. While everything else collapsed, gold owners watched their wealth multiply 23 times over.

The exact same conditions are forming again. Two simultaneous wars. Energy prices spiking. A national debt past $38 trillion.

But this time, there’s a wildcard that didn’t exist in the 1970s. The U.S. government owns 8,133 tonnes of gold, valued on the books at $42.22 per ounce. President Trump has the legal authority to correct it with an executive order.

When he does, it won’t just be a gold rally. It will be the largest wealth transfer in modern history. $7,000? $10,000? $20,000?

The smart money isn’t waiting to find out. They’re positioning now, like insiders, before the revaluation hits. That’s why I want you to read The Great Gold Reset.

| CLAIM YOUR FREE GREAT GOLD RESET REPORT → |

The IRS Shakeup + Inflation = One Conclusion for Retirees

The IRS enforcement gap and the inflationary surge are not competing stories. They are complementary. The IRS gap creates a window where certain legal rollovers and repositioning strategies face less scrutiny than normal. The inflation surge creates the urgency to use that window — because every month you wait, 0.6% of your purchasing power disappears.

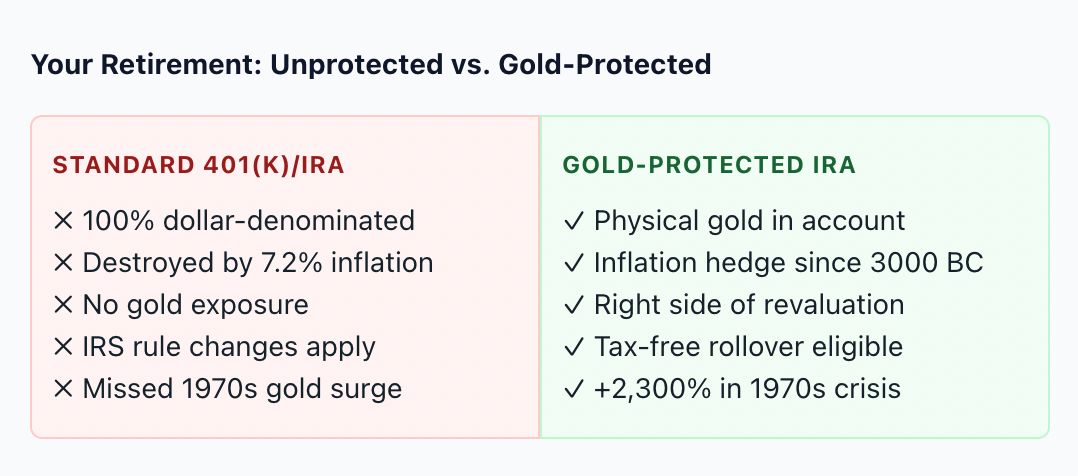

The Americans who are thinking clearly about this are doing two things simultaneously: using the legal IRS rollover mechanism to move a portion of their retirement into physical gold (tax-free, penalty-free), and positioning for the gold revaluation that the inflation trajectory is making increasingly likely.

Neither of these moves requires taking unnecessary risk. Both are IRS-approved. Both use existing tax law. And both produce dramatically different outcomes than leaving 100% of your retirement in dollar-denominated paper assets while inflation runs at 7.2% annualized and the government sits on a $42-per-ounce gold fiction.

Inflation Just Exploded 0.6% in ONE MONTH

March 2026: +0.6% inflation in a single month. If this pace continues, we’re looking at 7.2% annual inflation. The last time this happened, gold gained 2,300%. The stock market lost 92% of its real value.

The U.S. government owns 8,133 tonnes of gold valued at $42.22/oz. The market price is $6,000+. Trump has the legal authority to correct it with one signature. When he does, it will be the largest wealth transfer in modern history.

Two Windows. Both Closing. Act While You Still Can.

The IRS enforcement gap will not last forever. Eventually, the agency will be restaffed, the scrutiny will return, and the window for low-friction rollovers will tighten. The inflation trajectory will not wait for you to decide either — 0.6% per month compounds into serious purchasing power destruction within a year.