In 1934, the Government Repriced Gold and Transferred Billions Overnight. The Same Legal Authority Still Exists. And Your Credit Card Is Charging You 22.76% While You Wait.

The move Washington made in 1934

In 1934, the government executed a legal maneuver that transferred billions in wealth overnight. Most Americans had no idea it was coming. A small group who saw it early walked away wealthy. Everyone else paid for it.

Trump has the same legal authority today. Advisors close to the administration believe he’s considering using it. If he does, the transfer happens fast — and the window to be on the right side of it is already closing.

We put together a free report on exactly what this move is, why the timing points to now, and the one step ordinary Americans can take to position themselves before it happens.

It costs nothing. Takes 30 seconds to request. The people who moved early in 1934 didn’t have a warning. You do.

| 👉 Send me the free report |

On January 30, 1934, President Franklin D. Roosevelt signed the Gold Reserve Act. With one signature, he changed the statutory price of gold from $20.67 per ounce to $35 per ounce — a 69% increase. The Treasury, which had collected Americans’ gold through Executive Order 6102 the previous year at the lower price, immediately booked a profit of nearly $3 billion (roughly $70 billion in 2026 dollars). Citizens who had surrendered their gold at $20.67 received no additional compensation after the repricing. The paper dollars they held in exchange were instantly worth only 59 cents on the gold dollar.

The Federal Reserve Bank of New York’s Governor George Harrison noted at the time that the Gold Reserve Act “effectively stripped the Federal Reserve of its independent monetary policy role.” The Washington Post described it plainly: “The gold reserve act of 1934 not only took from the system all of its gold, but in doing so definitely deprived it of future control over gold movements.” The Treasury used the $3 billion profit to establish the Exchange Stabilization Fund — giving the executive branch power to control the dollar’s value without Congressional approval or Federal Reserve involvement.

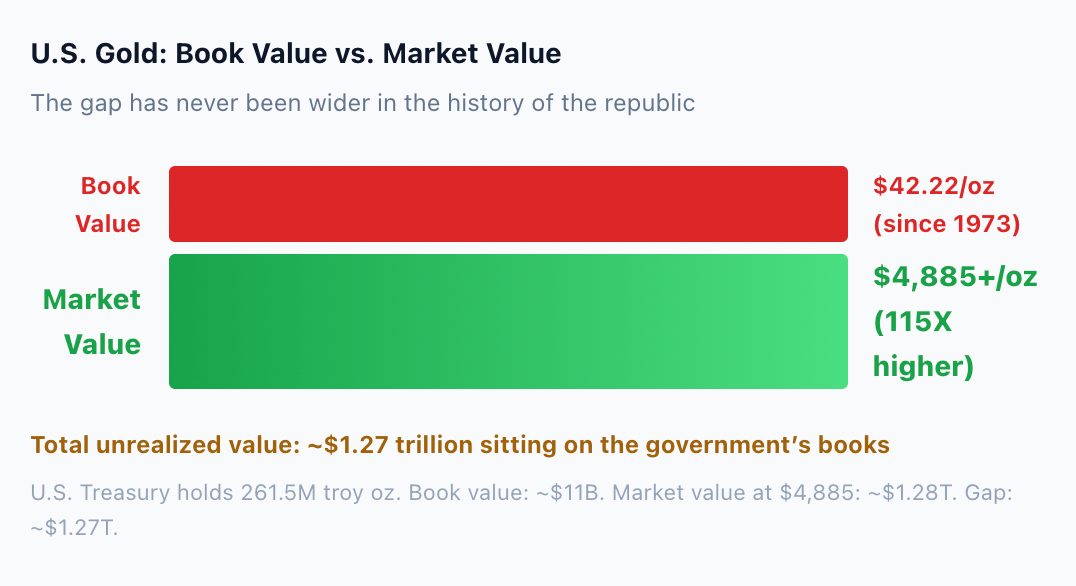

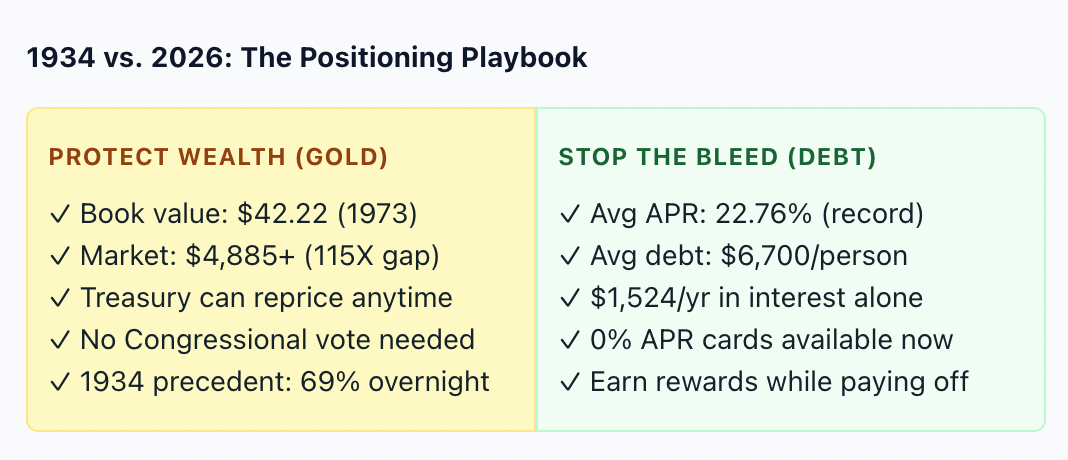

This was the largest wealth transfer in American history up to that point. A small group of people who understood what was coming — and held assets outside the paper dollar system — preserved their purchasing power. Everyone else absorbed the devaluation. The legal authority that made it possible did not expire. The Secretary of the Treasury still has the power to issue gold certificates at any price. And the gap between the government’s book value for gold and the market price is now 68 times wider than it was in 1934.

The parallels to 2026 are not theoretical.

(AD) They are documented. In 1934, the government executed a legal maneuver that transferred billions in wealth overnight. Most Americans had no idea it was coming. A small group who saw it early walked away wealthy. Everyone else paid for it. Trump has the same legal authority today. Advisors close to the administration believe he’s considering using it. If he does, the transfer happens fast — and the window to be on the right side of it is already closing. It costs nothing. Takes 30 seconds to request. The people who moved early in 1934 didn’t have a warning. You do. Send me the free report.

The 1934 Gap Was 1.69X. The 2026 Gap Is 115X. The Legal Authority Is Identical.

In August 2025, the Federal Reserve published a research note titled “Official Reserve Revaluations: The International Experience,” documenting how five countries monetized their gold reserves without selling a single ounce. Treasury Secretary Scott Bessent set off speculation in February when he said the administration would “monetise the assets listed in the federal budget.” He later clarified he “didn’t mean repricing gold.” But Bessent also said gold “cannot default, cannot suffer deficits.” Bank of America’s Francisco Blanch told Bloomberg that repricing gold would be “bullish for the gold market because it would show that gold is no longer this barbarous relic.” The conditions that made the 1934 move possible — excessive debt, a weakening currency, and political pressure to find revenue without raising taxes — are all present today, amplified by a factor of 68.

While You Wait for Washington to Act, Your Credit Card Is Quietly Draining $1,524 Per Year

The average American carries over $6,700 in credit card debt at an average APR of 22.76% — the highest rate in recorded history. Total U.S. credit card debt crossed $1.2 trillion in early 2026. Delinquency rates have risen for 11 consecutive quarters. At 22.76%, a $6,700 balance costs $1,524 per year in interest alone — $127 per month going directly to the bank, not your balance. Over three years, you would pay $4,573 in interest on a $6,700 debt, nearly 70% of the original amount.

The irony is painful: Americans are paying the highest credit card rates in history while simultaneously ignoring the tools that could eliminate them. A 0% introductory APR balance transfer card eliminates interest for 15-21 months. Every payment goes toward principal, not the bank’s profit margin. The Americans who use these tools save $1,500+ per year in interest — money that could be redirected toward building wealth, funding a gold IRA, or simply stabilizing their household finances during the most uncertain economic period since 2008.

The connection between the gold revaluation thesis and credit card debt is strategic: Americans who are losing $1,524 per year to credit card interest while simultaneously ignoring the tools to eliminate it are fighting with one hand tied behind their back. The smartest financial move in 2026 is addressing both sides: positioning for the gold revaluation that the $42.22 book value gap makes possible, and eliminating the 22.76% credit card drain that is eroding present-day wealth. The cards that offer both 0% intro APR on purchases and balance transfers while also earning rewards on every qualifying purchase are the ones that turn a defensive move into an offensive one.

Cards built for the Future. Ready Now.

If your money’s not working for you — it’s broken.

These cards don’t just offer 0% intro APR on purchases and balance transfers to help you escape debt. They also earn rewards on every qualifying purchase.

It’s built for smart users.

| See these top cards → |

This is an advertisement.

This email contains references to products from one or more of our advertisers. FinanceBuzz is an informational website that provides tips, advice, and recommendations to help you make financial decisions. We strive to provide up-to-date information, but make no warranties regarding the accuracy of our information.

Ultimately, you are responsible for your financial decisions. FinanceBuzz is not a financial institution and does not provide credit cards or any other financial products. FinanceBuzz does not make any credit decisions. We may receive compensation from the products and services mentioned in this email.

Please click here to opt out of future emails from FinanceBuzz. 111 E. Atlantic Ave., Suite 200 Delray Beach, FL 33444

The People Who Won in 1934 Did Two Things. You Can Do Both Right Now.

The Americans who emerged from the 1934 repricing on the right side did two things: they held assets outside the paper dollar system, and they minimized the drains on their present-day wealth. The same playbook applies in 2026 — but with better tools. Physical gold is legal to own (it wasn’t in 1934). Gold IRAs allow tax-advantaged holdings. And 0% intro APR cards did not exist in the 1930s. Today, you can position for the repricing and eliminate the credit card drain simultaneously. The people who moved early in 1934 had no warning. You have the data, the tools, and the historical precedent — all pointing in the same direction.

Cards built for the Future. Ready Now.

If your money’s not working for you — it’s broken. These cards don’t just offer 0% intro APR on purchases and balance transfers to help you escape debt. They also earn rewards on every qualifying purchase. It’s built for smart users.

Bottom Line

In 1934, the government executed a legal maneuver that transferred billions in wealth overnight. Roosevelt repriced gold from $20.67 to $35 per ounce — a 69% increase — and the Treasury booked a $3 billion profit while citizens who had surrendered their gold received paper dollars instantly worth 59 cents on the gold dollar. The legal authority that made it possible did not expire. The Secretary of the Treasury can still issue gold certificates at any price without a Congressional vote. And the gap between the government’s book value ($42.22, set in 1973) and the market price ($4,885+) is now 115X — compared to just 1.69X in 1934.

The conditions that made the 1934 move possible are all present today, amplified dramatically. The national debt stands at $39 trillion with $1 trillion in annual interest. The Fed just fractured 8-4 — the first 4-member dissent since 1992. A new Fed chair takes over in weeks. Treasury Secretary Bessent said the administration would “monetise the assets listed in the federal budget.” The Fed’s own research documented how five countries monetized gold reserves without selling a single ounce. Trump has the same legal authority today. Advisors close to the administration believe he’s considering using it. The people who moved early in 1934 didn’t have a warning. You do.

Meanwhile, the average American carries over $6,700 in credit card debt at 22.76% APR — the highest rate in recorded history — costing $1,524 per year in interest alone while total U.S. credit card debt has crossed $1.2 trillion. If your money’s not working for you — it’s broken. These cards don’t just offer 0% intro APR on purchases and balance transfers to help you escape debt. They also earn rewards on every qualifying purchase. Every dollar saved on credit card interest is a dollar that can be redirected toward positioning for what’s coming.

The 1934 winners did two things: they held assets outside the paper dollar system, and they minimized the drains on their present-day wealth. The 2026 playbook is identical but the tools are better — physical gold is legal to own, Gold IRAs provide tax-advantaged protection, and 0% intro APR cards eliminate the credit card drain that erodes present-day wealth. Both moves are available right now. Both cost nothing to explore. And both windows close on their own timelines — the gold repricing window when Washington acts, and the 0% APR window when introductory offers expire. The data, the tools, and the historical precedent all point in the same direction.