$265 Billion Trapped: Wall Street Sold You "Democratized" Credit. Now They Won't Let You Leave.

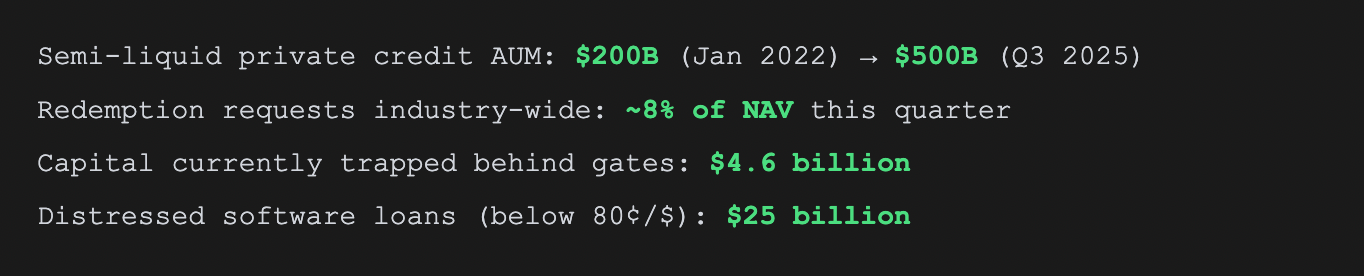

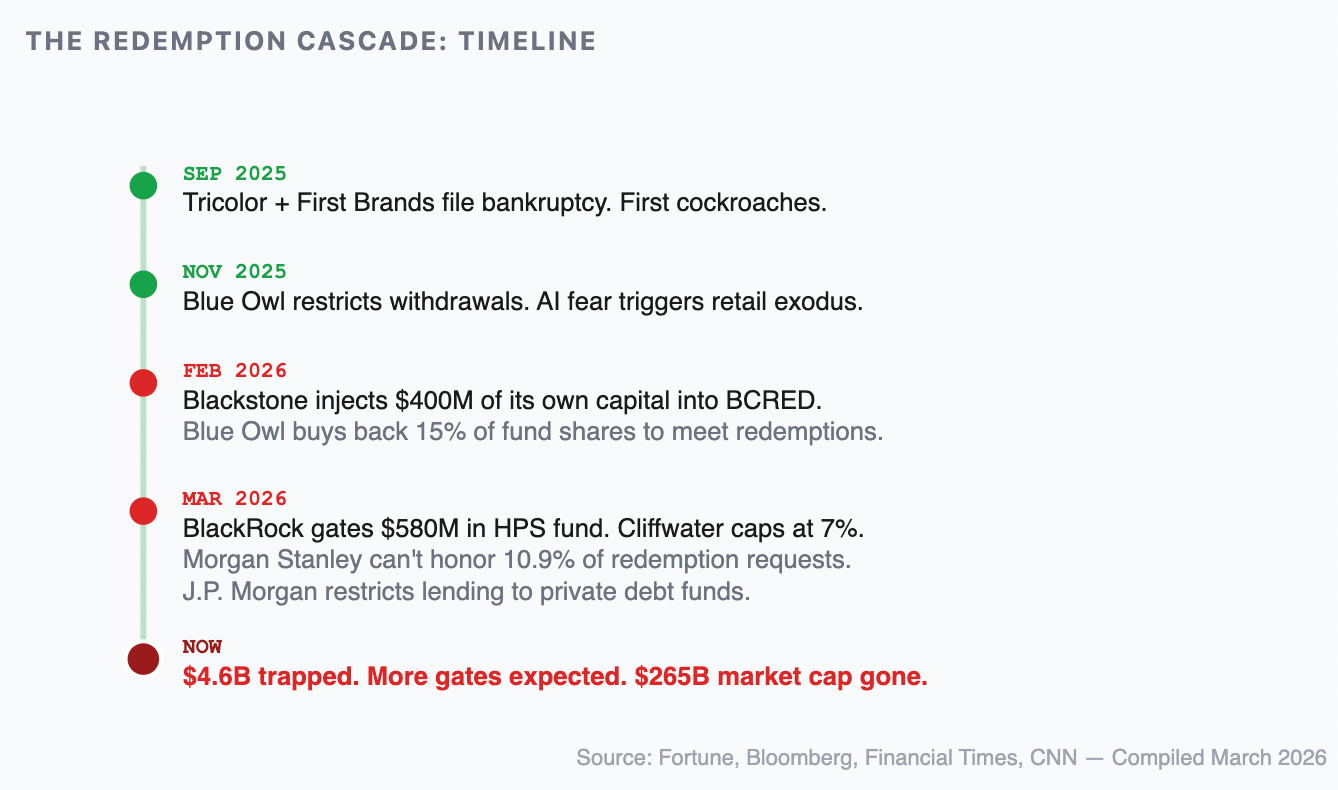

Blue Owl lost two-thirds of its value. Blackstone injected $400M of its own cash to stop a bank run. BlackRock gated $580M in redemptions. And $4.6 billion in investor capital is stuck behind withdrawal limits right now. Here's what happened, why it matters to you, and the three trades I'm watching.

I need to be direct with you.

If you own shares in any private credit fund — a BDC, a "semi-liquid" vehicle, anything marketed as giving you "institutional-grade" access to private debt — you need to read this entire piece. Because the exit door is closing, and for some investors, it already has.

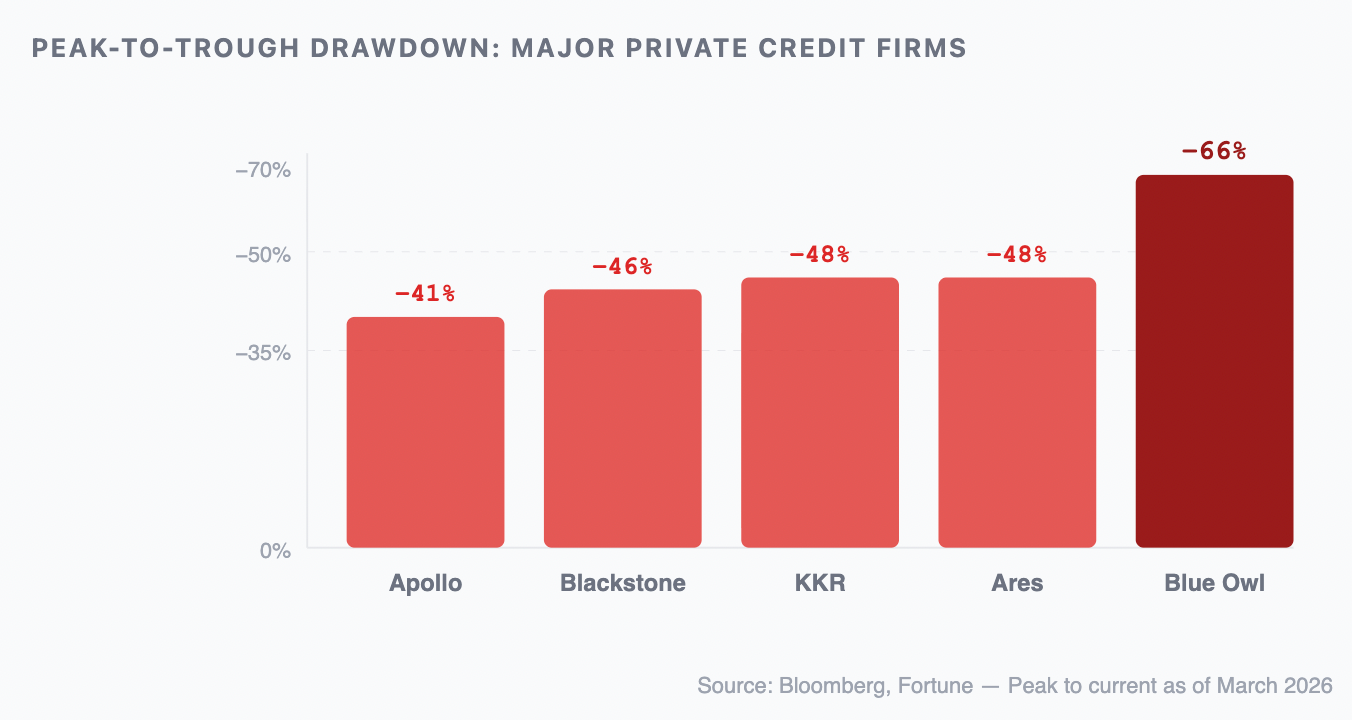

Over the past six months, the five largest alternative asset managers — Blackstone, KKR, Apollo, Ares, and Blue Owl — have collectively lost $265 billion in market capitalization. That's not a slow bleed. That's a wipeout.

The speed of this unwind is what makes it different from 2008. In the mortgage crisis, the blowup took 18 months to cascade from subprime to prime. Here, the AI disruption thesis hit private credit lending books within weeks. Software companies underwritten at 24x revenue multiples in 2023 are now trading at 18x — and some face outright obsolescence from generative AI tools. The collateral is evaporating in real time.

How "Democratization" Became a Trap

For decades, private credit was exclusively institutional. Pension funds. Endowments. Family offices. People who understood that locking up capital for 8–10 years was the price of admission.

Then the PE titans discovered retail. Blue Owl built 40% of its $300 billion in AUM from individual investors. Blackstone's BCRED fund advertised 9.8% annual returns. Morgan Stanley called it "democratizing access." It sounded great.

The catch was in the fine print: these "semi-liquid" funds cap withdrawals at 5% of NAV per quarter. When everything is going up, nobody reads that clause. When everything is going down, that clause is the only thing that matters.

Jamie Dimon said it plainly last September: when "cockroaches" like Tricolor surface, more are lurking. He was right. The cockroaches multiplied.

Why This Matters Even If You Don't Own Private Credit

You might be reading this thinking: I don't own any BDCs or private credit funds. Why should I care?

Because the contagion path is already visible.

U.S. banks have extended roughly $300 billion in loans to private credit providers, according to Moody's. If those providers face a wave of forced selling to meet redemptions, the losses flow back into the banking system. Banks tighten lending. Consumers and small businesses get squeezed. We've seen this movie before — it was called 2008.

Bank of America's analysts said there was "misinformation" causing overreaction. Private fund managers say the fears are overblown. They may be right. But the pattern is always the same: the people telling you not to panic are the ones who lose the most if you do.

Here's a number worth watching: $25 billion in software-sector loans now trade below the distress threshold of 80 cents on the dollar. Bloomberg found at least 250 loans worth $9 billion were miscategorized as "other industries" by BDCs to hide the true software concentration. The sector exposure is deeper than the public numbers suggest.

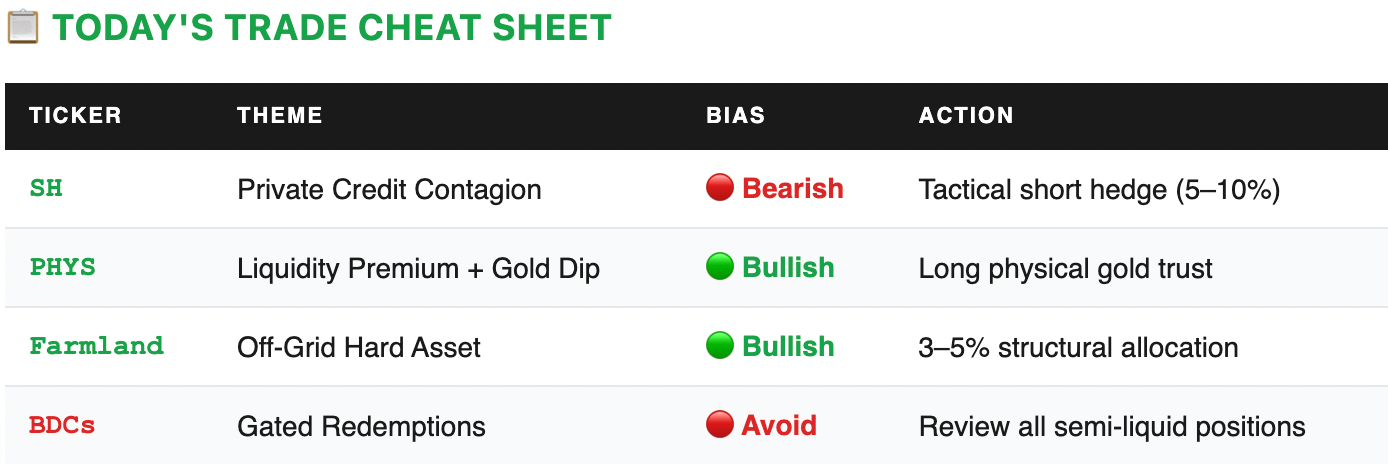

Ticker: SH — ProShares Short S&P 500

Thesis: If private credit stress bleeds into bank lending, the broader market takes a hit. SH provides a tactical short position without options complexity. Size it as a hedge (5–10% of portfolio), not a bet.

Where the Smart Money Is Going

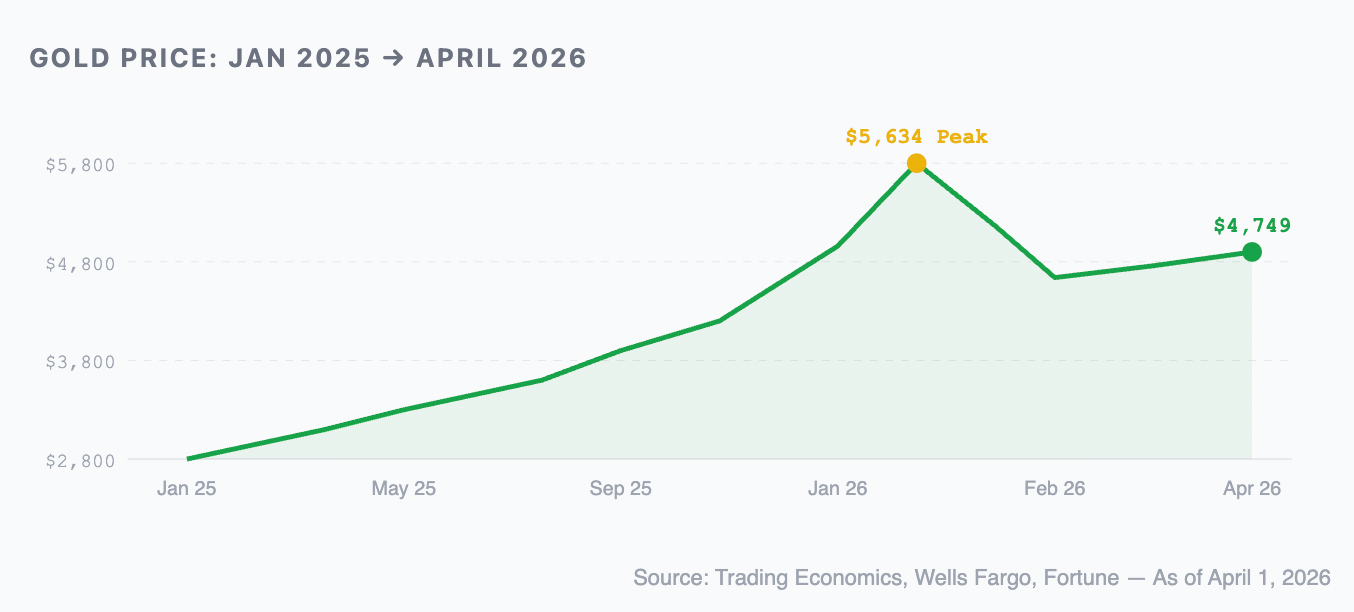

Gold is at $4,749 per ounce today. Down from the January peak above $5,600, but still up 46% year-over-year. Wells Fargo just raised their year-end target to $6,100–$6,300. JPMorgan is at $6,300. UBS at $6,200.

The thesis is straightforward: central banks are still buying (China's PBOC has bought gold for 15 consecutive months), the Fed is projecting only one rate cut this year, and geopolitical risk from the Iran situation isn't going away.

But the private credit blowup adds a new layer. When "semi-liquid" becomes illiquid, investors rediscover why fully liquid, unencumbered hard assets matter. You can sell an ounce of gold any day of the week. Try doing that with a gated BDC.

Ticker: PHYS — Sprott Physical Gold Trust

Thesis: Fully allocated physical bullion. No counterparty risk. No withdrawal gates. No "semi-liquid" fine print. Gold's 17% pullback from the January peak is the entry point Wells Fargo is telling you to buy.

The Third Trade: Don't Ignore Farmland

I keep coming back to this: the assets that can't be gated, frozen, or debased with a keystroke are the ones that will matter most over the next decade. Farmland is one of them.

You can't redeem farmland at 5% per quarter because it's not held in a fund with a withdrawal gate. You can't mark it down because a software company lost its revenue to Claude or ChatGPT. It produces income from a commodity people physically need, and its value is negatively correlated with the financial system's instability.

Asset: Farmland — via AcreTrader or FarmTogether

Thesis: Non-bank, non-digital, non-gatable. A productive hard asset that generates income regardless of what happens in software lending markets. Consider a 3–5% allocation as structural diversification away from anything with a withdrawal clause.